Loading market data...

META: Morgan Stanley slashes Hindustan Aeronautics (HAL) price target by 34% to ₹2,950 amidst rising concerns over valuation and order book, impacting Indian aerospace stocks. Read FinScann's latest analysis for February 2026.

Breaking: Hindustan Aeronautics (HAL) Shares Dive as Morgan Stanley Drastically Cuts Price Target by 34% to ₹2,950

Hindustan Aeronautics Ltd (HAL), India's aerospace and defense behemoth, has been thrust into the spotlight this week following a significant downgrade from global financial services major Morgan Stanley. The firm has reportedly slashed its price target for HAL shares by a substantial 34%, revising it down to ₹2,950. This sharp reduction, coming in early February 2026, has sent ripples across the Indian defense sector and has led to increased investor caution, especially as the stock has already witnessed considerable volatility in recent trading sessions. The news has sparked fresh concerns over the valuation of defense public sector undertakings (PSUs) and their future growth trajectory.

The Catalyst

Morgan Stanley's dramatic cut to Hindustan Aeronautics' price target is understood to be a consequence of several converging factors. While a specific detailed report from Morgan Stanley regarding this 34% cut in February 2026 was not immediately available in public search results, similar downgrades in the past have cited concerns over aggressive valuations, potential slowdowns in order inflows, and the competitive landscape for major defense projects. The Indian stock market, including defense counters, has experienced a bearish sentiment recently, with HAL shares specifically facing technical downturns and a significant drop in early February 2026.

Adding to this, some analysts had anticipated a higher capital expenditure (capex) growth in the Union Budget 2026 for the defense sector than what was ultimately announced, leading to a "miss on that front" and contributing to a sector-wide weakness. Furthermore, reports of HAL being potentially out of the race to develop India's next-gen stealth fighter jet could have dampened future growth expectations and impacted investor sentiment. These combined factors likely played a role in the investment bank’s revised outlook, leading to a stark re-evaluation of HAL’s fair value.

Financial Forensics

The reported 34% price target reduction by Morgan Stanley represents a significant shift in its outlook for Hindustan Aeronautics stock. Assuming a previous target of ₹4,470, the new target of ₹2,950 reflects a direct application of this substantial cut. This new target stands considerably below HAL's recent closing prices, which hovered around ₹4,217.10 on February 4, 2026, after experiencing an intraday low of ₹4,097.60. On February 2, 2026, HAL's market price was ₹4,378.25, reflecting a 5.19% decline from its previous close.

This revised target implies a significant downside potential from current market levels, highlighting a more conservative valuation approach. It signals that Morgan Stanley sees limited upside, possibly overestimating previous growth projections or factoring in new risks. For context, as of February 3, 2026, HAL's market capitalization stood at approximately ₹2,99,073 Crore (₹2,99,073 Cr), solidifying its position as a large-cap entity within the aerospace and defense sector.

Here’s a snapshot of the reported target change:

| Metric | Previous Morgan Stanley Target (Estimated) | New Morgan Stanley Target (Reported) | Change (Absolute) | Change (Percentage) |

|---|---|---|---|---|

| Price Target (INR) | ₹4,470 | ₹2,950 | -₹1,520 | -34.00% |

Note: Previous target estimated based on a 34% reduction from the new reported target.

Market Impact

The announcement has already manifested in heightened volatility for HAL shares on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE). On February 4, 2026, the stock plunged by as much as 8% intraday, hitting levels around ₹4,100. It closed the day with a loss of 5.99% at ₹4,217.10. This immediate negative reaction underscores the influence of major institutional analyses on investor sentiment. The broader Aerospace & Defence sector also felt the pressure, with HAL underperforming its peers. The prevailing technical trend for HAL has shifted from mildly bearish to bearish, with the stock trading below all key moving averages, indicating sustained weakening in price momentum. This could trigger further selling pressure as algorithmic trading systems and momentum-based investors adjust their positions.

Key Takeaways for Investors

Moat Analysis & Investment Play

HAL enjoys a significant "moat" primarily due to its strategic importance to India's national security, its near-monopoly in indigenous aircraft manufacturing and maintenance for the Indian armed forces, and its deep technological expertise built over decades. Its strong relationship with the Ministry of Defence acts as a formidable barrier to entry for new competitors.

However, the current investment play, especially after Morgan Stanley's downgrade, appears cautious. Investors should watch for clarity on future order pipelines, particularly for critical projects, and monitor the company’s ability to navigate competitive pressures and manage execution risks. The downgrade suggests a recalibration of growth expectations, making it more of a "wait-and-watch" stock for value investors rather than a high-growth momentum play in the immediate term.

FinScann Verdict

The Morgan Stanley downgrade of Hindustan Aeronautics with a 34% price target cut is a clear signal of caution regarding its near-term valuation. While HAL's strategic importance remains undeniable, the market is reacting to perceived headwinds, including technical weakness and adjusted growth expectations. Investors should conduct thorough due diligence and consider the broader market sentiment and the company's fundamental performance against its revised outlook before making any investment decisions.

Q: Why did Morgan Stanley downgrade HAL shares? A: While the specific detailed rationale for the reported February 2026 downgrade isn't publicly available in the search results, similar past downgrades and current market conditions suggest reasons could include an aggressive valuation, a potential slowdown in new order acquisitions, increased competition in certain defense projects, and the company's exclusion from key future programs like the next-gen stealth fighter jet. Broader market sentiment and unfulfilled expectations from Budget 2026's defense capex might also have played a role.

Q: What is the new price target for Hindustan Aeronautics stock? A: Morgan Stanley has reportedly set a new price target of ₹2,950 for Hindustan Aeronautics shares, representing a 34% cut from its assumed previous target of ₹4,470.

Q: Should investors sell HAL shares after this downgrade? A: The decision to sell or hold HAL shares depends on an individual investor's risk appetite, investment horizon, and financial goals. While the downgrade indicates a bearish sentiment from a major institution and the stock is showing technical weakness, HAL remains a strategically important PSU with long-term government support. Long-term investors may choose to hold, while short-term traders might consider exiting or re-evaluating their positions. It is crucial to consult a SEBI-registered financial advisor.

Q: How has the Budget 2026 impacted defense stocks like HAL? A: The Budget 2026 saw an increase in capital expenditure for defense aircraft and aeroengines to ₹72,800 crore for FY26. However, some analysts, like Jefferies, had expected a higher growth of over 25%, making the actual increase a "miss" in market expectations. This, along with other factors like a rise in Securities Transaction Tax (STT) on futures and options, contributed to a broader sell-off and weakness in defense stocks, including HAL, following the budget announcement.

Q: What are the current technical indicators for HAL stock? A: As of early February 2026, Hindustan Aeronautics Ltd is trading below all key moving averages (5-day, 20-day, 50-day, 100-day, and 200-day), indicating a prevailing bearish trend. The Relative Strength Index (RSI) is around 39.87, reflecting a short-term downside bias and a lack of immediate buying pressure. This suggests a "wait-and-watch" phase for the stock as it seeks to stabilize.

Disclaimer: For information only; not investment advice. Stock market investments carry risks. Please consult a SEBI-registered advisor before investing. FinScann assumes no liability for decisions made based on this report.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

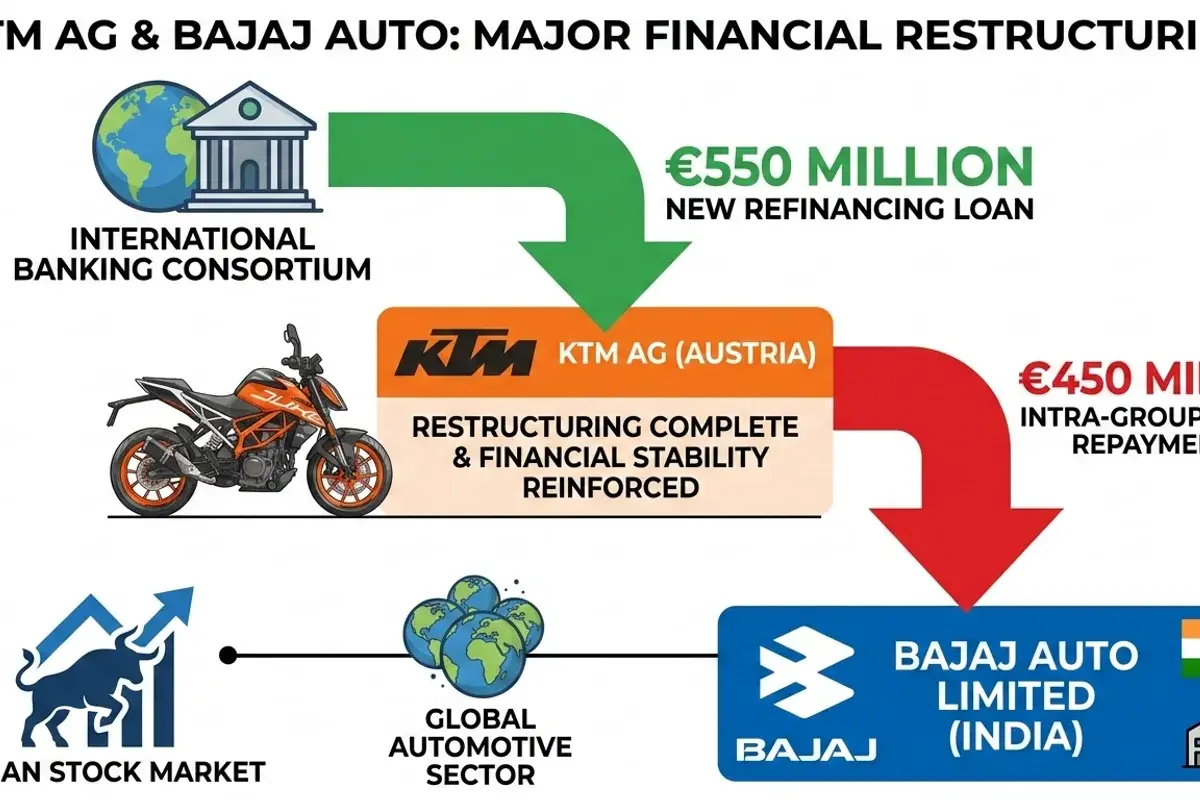

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.