Loading market data...

META: Suzlon Energy shares saw a 1.67% dip on February 5, 2026, reacting to its Q3 FY26 results amid broader market pressure. FinScann analyzes the company's financials, market performance, and outlook for investors.

Suzlon Energy Shares See Muted Response, Dip 1.67% Post Q3 FY26 Results Amid Broader Market Sell-off

Suzlon Energy Ltd. (NSE: SUZLON, BSE: 532667) witnessed its shares dip by 1.67% on February 5, 2026, settling near ₹48.63 on the National Stock Exchange (NSE) during early trading hours. This reaction came directly after the wind energy major announced its financial results for the third quarter of Fiscal Year 2026 (Q3 FY26), ending December 31, 2025. The slight decline in Suzlon shares occurred amidst a broader market downturn, with the Nifty 50 trading below 25700 and the overall renewable energy sector also experiencing a decline.

The Catalyst

The immediate catalyst for the market's subdued response to Suzlon's stock on February 5, 2026, was the announcement of its Q3 FY26 financial results. While the company reported robust year-on-year growth in both revenue and profit, market expectations, possibly fueled by optimistic analyst previews, appeared to have been set higher. The broader market sentiment, marked by a significant Sensex decline of over 450 points and a 2.18% drop in the renewable energy sector, also contributed to the pressure on Suzlon's stock. Investors were closely watching the Suzlon Q3 results for signs of sustained growth and execution momentum in India's expanding renewable energy landscape.

Financial Forensics

Suzlon Energy reported a solid increase in its financial performance for Q3 FY26. The company's consolidated Profit After Tax (PAT) rose by 14.83% year-on-year (YoY) to ₹445.28 crore, compared to ₹387.76 crore in the corresponding quarter of the previous fiscal year (Q3 FY25).

Revenue from operations also saw a significant surge, climbing 42.42% YoY to ₹4,228.18 crore in Q3 FY26, up from ₹2,968.81 crore in Q3 FY25. This demonstrates strong operational execution and increased dispatches of wind turbine generators.

Despite this impressive YoY growth, market expectations, as per some analyst previews, might have been even higher. Earlier estimates by some analysts had projected a potential 91% rise in PAT and a 100% rise in EBITDA for Suzlon's Q3 FY26. While Nuvama had a 'hold' rating and expected execution of 740MW and margins around 18%, JM Financial, with a 'buy' rating, had predicted a 40% YoY profit rise but noted a potential 58% quarter-on-quarter (QoQ) decline in profit for the December 2025 quarter. The reported PAT of ₹445.28 crore, while strong YoY, may have fallen short of some of the more bullish expectations, particularly on a QoQ basis, which contributed to the muted stock reaction.

Here’s a comparison of Suzlon's Q3 FY26 performance:

| Financial Metric (₹ Crore) | Q3 FY26 (Actual) | Q3 FY25 (Actual) | YoY Change (%) | Analyst Expectations (Range) |

|---|---|---|---|---|

| Revenue from Operations | 4,228.18 | 2,968.81 | +42.42% | 3,993.7 Cr - 4,690 Cr (up 34-58% YoY) |

| Consolidated PAT | 445.28 | 387.76 | +14.83% | 387 Cr - 557.6 Cr (up 40-91% YoY) |

| EBITDA (Estimated) | ~700.8 (JM Financial) | ~500.6 (Implied, Q3 FY25) | ~+40% | 700.8 Cr - 923.8 Cr (up 40-100% YoY) |

(Note: EBITDA for Q3 FY25 is an estimate based on reported YoY growth and Q3 FY26 estimates.)

Market Impact

On February 5, 2026, Suzlon shares closed at ₹48.63, marking a 1.67% decline from its previous close. This performance underperformed the benchmark Sensex, which fell by 0.47%, and the broader Renewable Energy sector, which dropped by 2.18% on the same day. The stock opened at ₹50.00, touching an intraday high of ₹50.02 before retreating to a low of ₹48.62. The trading session saw a significant volume of 1.84 crore shares changing hands, indicating strong investor activity despite the price dip.

It is crucial to note that this dip comes after a remarkable three-day rally where Suzlon Energy's stock had gained approximately 8% cumulatively and had added 3.2% in February alone, hitting a three-week high of ₹50 on February 4, 2026. This pre-results surge suggests that a significant portion of the positive sentiment regarding strong earnings was already factored into the stock price. The post-results decline, therefore, could be interpreted as a "sell-on-news" event or a recalibration by the market based on the actual numbers relative to heightened expectations.

Moat Analysis: Suzlon's Positioning

Suzlon Energy operates in a sector critical to India's energy transition. Its "moat" primarily derives from its vertically integrated business model, covering design, manufacturing of key components like rotor blades, generators, and control equipment, as well as project execution and long-term operation & maintenance (O&M) services. With over 30 years of experience and 21 GW of wind energy installed across 17 countries, Suzlon is a leader in India's wind energy sector, managing 15.1 GW of domestic wind assets. This extensive experience and established infrastructure create high barriers to entry for new competitors. The company's focus on improving its order book, strengthening project execution, and building long-term service contracts further enhances its competitive edge and provides stable revenue streams.

Key Takeaways for Investors

FinScann Verdict

Suzlon Energy's Q3 FY26 results demonstrate healthy operational growth, aligned with India's ambitious renewable energy targets. The 1.67% dip in Suzlon shares on the day of results, while a notable reaction, appears to be a recalibration against potentially elevated market expectations and general market softness. For long-term investors bullish on India's green energy transition, any significant correction could present a buying opportunity, given Suzlon's established market position and improving financials.

Q: Why did Suzlon shares decline despite reporting profit growth? A: Suzlon Energy reported a 14.83% increase in consolidated PAT and a 42.42% rise in revenue year-on-year for Q3 FY26. However, the share price dipped by 1.67% on February 5, 2026, likely due to market expectations being even higher than the reported strong growth, or concerns over potential sequential profit decline flagged by some analysts. The broader market also saw a downturn on the day.

Q: What are the key financial highlights from Suzlon's Q3 FY26 results? A: For Q3 FY26 (December 2025 quarter), Suzlon Energy reported a consolidated Profit After Tax (PAT) of ₹445.28 crore, up 14.83% from Q3 FY25. Its revenue from operations reached ₹4,228.18 crore, marking a 42.42% increase year-on-year.

Q: How is the broader renewable energy sector performing in India? A: India's renewable energy sector is experiencing significant growth, with renewables, hydro, and nuclear contributing over 51% of the country's installed power capacity. However, the sector faced a 2.18% decline on February 5, 2026, reflecting general market pressures. The Union Budget 2026 offered fragmented support, with stagnant wind energy funding and reduced allocations for transmission and storage.

Q: What is the outlook for Suzlon Energy shares in 2026? A: Analysts generally maintain a positive outlook for Suzlon, with consensus "strong buy" ratings and average price targets around ₹70.82 for 2026. Expected steady growth in the renewable energy sector, improving order books, and a focus on project execution are key drivers. However, investor caution may stem from broader market volatility and specific budget allocations for wind energy infrastructure.

Disclaimer: For information only; not investment advice. Stock market investments carry risks. Please consult a SEBI-registered advisor before investing. FinScann assumes no liability for decisions made based on this report.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

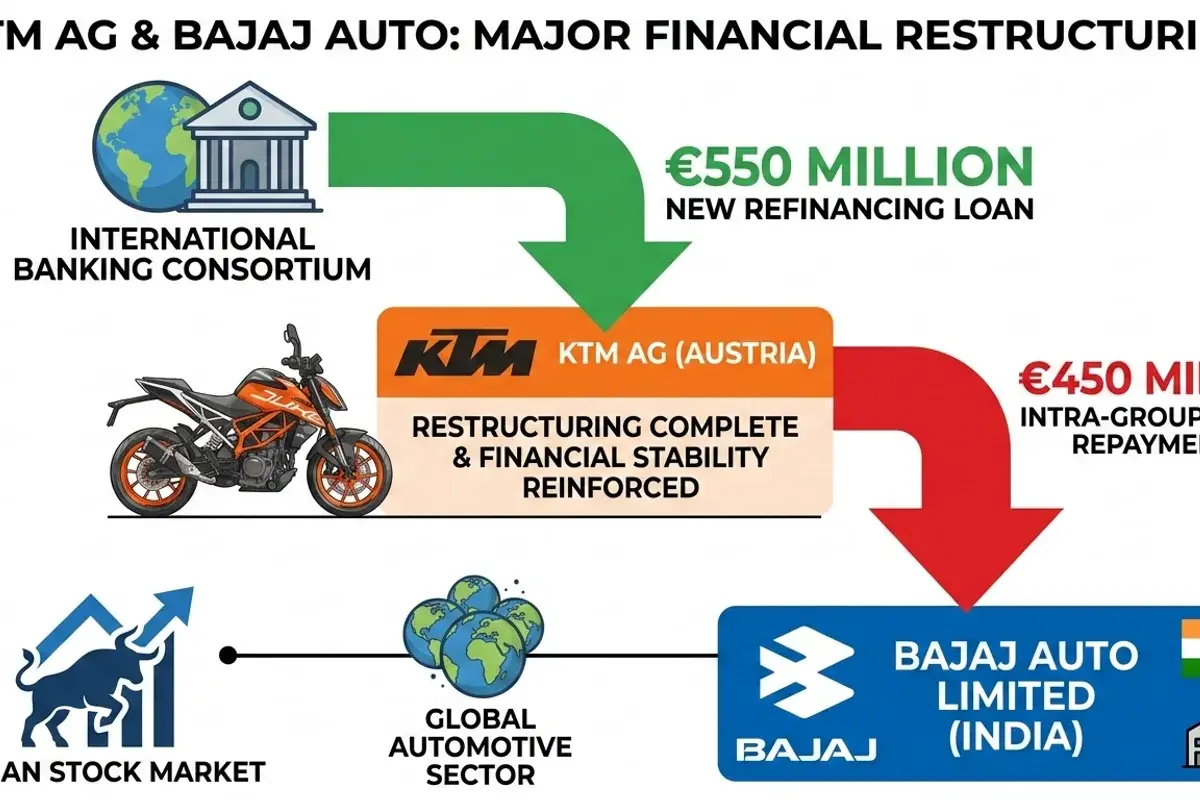

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.