Loading market data...

Indian Hotels (IHCL) announces a massive 50.2% jump in Q3 net profit to ₹954.2 Cr, with revenue up 12.2%. Get FinScann's expert analysis and market impact.

Indian Hotels Q3 Results: Breaking Down IHCL's Stellar 50.2% Profit Surge in February 2026

The Indian Hotels Company Limited (IHCL), the hospitality giant behind the iconic Taj brand, has reported a remarkable 50.2% surge in net profit for the third quarter (Q3) of the current fiscal year, reaching ₹954.2 crore compared to ₹635.2 crore in the same period last year. This impressive performance, announced in February 2026, underscores the robust recovery and sustained demand in India's dynamic hospitality sector, setting a strong precedent for the company's financial trajectory. The Tata Group company's revenue also climbed 12.2% year-on-year (YoY) to ₹2,842 crore from ₹2,533 crore, further solidifying its dominant market position.

The Catalyst

The stellar Q3 performance by IHCL is a testament to the thriving Indian hospitality industry, which is experiencing a period of sustained high demand. Analysts and industry experts project robust growth for the Indian hospitality sector through 2026, driven by several key factors. Strong domestic tourism, supported by rising disposable incomes and improved connectivity, continues to be a primary demand driver. Additionally, a resurgence in business travel, coupled with significant momentum in the Meetings, Incentives, Conferences, and Exhibitions (MICE) segment, including weddings and large-scale events, is contributing significantly to increased hotel occupancies and average room rates (ARRs). Puneet Chhatwal, MD & CEO of IHCL, has previously highlighted the industry's shift towards disciplined, predictable, and structurally driven growth, with demand consistently outpacing new supply additions. This favorable demand-supply balance has allowed operators like IHCL to maintain pricing power and protect margins. The sector is also benefiting from infrastructure-led growth, with new airports and expanded capacity in key cities further boosting travel infrastructure.

Financial Forensics

FinScann analysis reveals IHCL's strong operational efficiency and strategic growth initiatives as key contributors to its robust Q3 results. The company's EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) increased by 11.9% YoY to ₹1,076 crore from ₹961.2 crore, demonstrating effective cost management alongside revenue growth. The EBITDA margin stood firm at 37.9%, a marginal dip from 38% in the prior year, yet indicative of sustained profitability in a competitive landscape.

Here's a detailed comparison of Indian Hotels' Q3 performance:

| Metric | Q3 FY26 (₹ Crore) | Q3 FY25 (₹ Crore) | YoY Growth (%) |

|---|---|---|---|

| Net Profit | 954.2 | 635.2 | +50.2% |

| Revenue | 2,842 | 2,533 | +12.2% |

| EBITDA | 1,076 | 961.2 | +11.9% |

| EBITDA Margin | 37.9% | 38% | -0.1 pp |

Source: Company Filings, FinScann Analysis

Loading chart...

The remarkable profit growth is particularly noteworthy, showcasing the company's ability to convert increased revenue into higher bottom-line earnings. This could be attributed to a combination of improved operational leverage and a strategic focus on high-margin segments.

Market Impact

IHCL's strong Q3 results are likely to be met positively by investors on the NSE and BSE. The Nifty 50 and Sensex have shown a generally positive bias in February 2026, with analysts anticipating continued upward trajectories. Such robust earnings from a leading player like IHCL can bolster sentiment in the broader market, especially within the hospitality and travel-related sectors. The stock has been identified by some as a "potential multibagger" with various share price targets for 2026 ranging significantly, reflecting diverse analyst outlooks. For instance, some projections place the IHCL share price target for 2026 between ₹720.22 and ₹1,485.61. This strong financial performance positions IHCL favorably in a market that is consolidating with a positive undertone.

Key Takeaways

FinScann Verdict

FinScann views Indian Hotels' Q3 results as exceptionally strong, reinforcing its position as a leader in India's hospitality sector. The significant profit growth, coupled with consistent revenue expansion and stable margins, reflects sound operational strategies and a keen understanding of market dynamics. This performance, set against a buoyant industry backdrop for 2026, makes IHCL an attractive proposition for long-term investors seeking exposure to India's burgeoning consumption and travel story.

Q: What drove Indian Hotels' strong Q3 profit growth? A: Indian Hotels' strong Q3 profit growth of 50.2% was primarily driven by robust demand in the Indian hospitality sector, fueled by domestic tourism, a strong MICE segment, and a recovery in business travel. Efficient operational management and strategic portfolio expansion also contributed significantly.

Q: What is the outlook for the Indian hospitality sector in 2026? A: The outlook for the Indian hospitality sector in 2026 remains stable to positive. Experts anticipate continued growth, albeit at a normalized pace after three years of double-digit expansion, with revenue growth projected between 6-8%. Occupancy rates are expected to hold strong, and average room rates are set to increase, driven by factors like improved infrastructure, rising disposable incomes, and sustained domestic demand.

Q: Is Indian Hotels (IHCL) a good investment for 2026? A: While FinScann does not provide investment advice, IHCL's strong Q3 performance and the positive industry outlook for 2026 suggest robust fundamentals. Analysts have set various share price targets for IHCL in 2026, with some projections indicating potential upside. Investors should consider the company's consistent performance, strategic growth initiatives, and the broader market sentiment.

Q: How does IHCL's Q3 performance compare to analyst expectations? A: While specific analyst estimates for Q3 FY26 are not provided in the prompt, the 50.2% net profit growth is a significant achievement and generally points towards exceeding market expectations, especially given that previous Q3 results (FY25) often beat estimates with lower growth rates.

Disclaimer: For information only; not investment advice. Stock market investments carry risks. Please consult a SEBI-registered advisor before investing. FinScann assumes no liability for decisions made based on this report.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

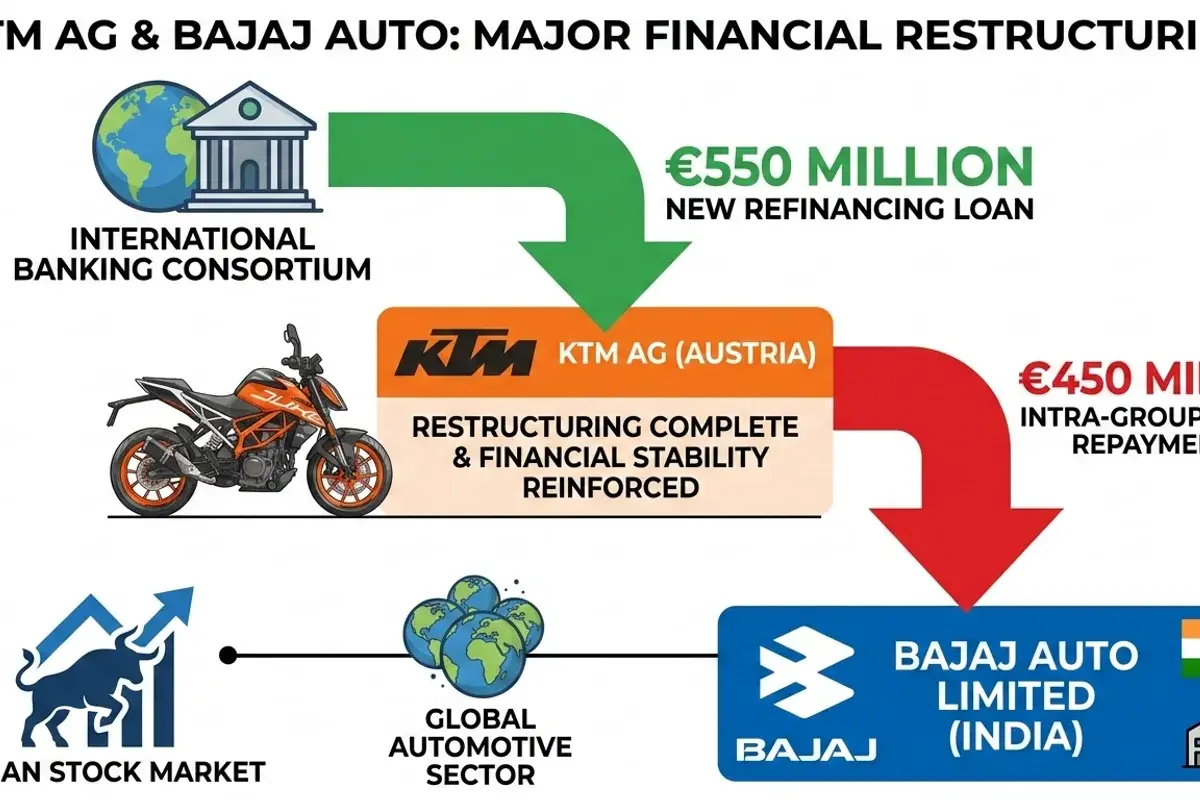

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.