Loading market data...

FinScann analyzes the Ministry of Defence's ₹2,312 Cr deal with HAL for 8 Dornier aircraft, examining market impact, HAL's Q3 results, and India's booming defence sector in February 2026.

HAL Soars: MoD Seals ₹2,312 Crore Dornier Aircraft Deal, Boosting Defence Stocks & Make in India Ambitions (February 2026 Analysis)

In a landmark move on February 12, 2026, the Ministry of Defence (MoD) signed a substantial contract worth ₹2,312 crore with state-owned aerospace major Hindustan Aeronautics Limited (HAL) for the procurement of eight Dornier 228 aircraft. This critical acquisition, destined for the Indian Coast Guard (ICG), is set to significantly bolster India's maritime surveillance capabilities and provides a major fillip to the nation's indigenous defence manufacturing ecosystem under the 'Buy (Indian)' category. The announcement comes just as HAL reported robust Q3 FY26 earnings, signaling strong operational momentum in the burgeoning Indian defence sector.

The Catalyst

The ₹2,312 crore deal for the Dornier 228 aircraft represents a strategic imperative for India's national security and its ambitious 'Aatmanirbhar Bharat' (self-reliant India) initiative. The eight Dornier 228 aircraft, equipped with advanced Operational Role Equipment, will enhance the Indian Coast Guard's ability to conduct crucial surveillance, search and rescue operations, and maritime patrols along India's extensive coastline. This contract directly supports the government's steadfast commitment to strengthening indigenous defence production and reducing reliance on foreign imports. The programme is expected to generate significant direct and indirect employment, fostering growth across HAL's production ecosystem and supporting a broad network of Micro, Small, and Medium Enterprises (MSMEs) and ancillary industries.

Financial Forensics

HAL's financials continue to demonstrate robust health, further reinforced by this significant MoD deal. The company recently announced a stellar performance for the third quarter of Fiscal Year 2026 (Q3 FY26), ending December 31, 2025. HAL reported a 30.3% year-on-year (YoY) jump in consolidated net profit to ₹1,867 crore, comfortably exceeding analyst expectations. Revenue from operations also saw a healthy increase of 10.7% YoY, reaching ₹7,699 crore in Q3 FY26.

This strong financial showing is complemented by a substantial and visible order book. As of early February 2026, HAL's order book stood at over ₹94,000 crore, providing robust revenue visibility well into 2032. This new ₹2,312 crore contract will further augment this impressive backlog, solidifying HAL's long-term growth trajectory. Furthermore, HAL declared a first interim dividend of ₹35 per equity share for FY26, with the record date set for February 18, 2026, and payment due by March 14, 2026.

Comparison: HAL's Key Financials (Q3 FY25 vs. Q3 FY26)

| Metric | Q3 FY25 (₹ Crore) | Q3 FY26 (₹ Crore) | YoY Change (%) |

|---|---|---|---|

| Revenue from Operations | ₹6,957 | ₹7,699 | +10.7% |

| Net Profit | ₹1,433 | ₹1,867 | +30.3% |

| Interim Dividend per Share | - | ₹35 | N/A |

| Order Book (Approx.) | N/A | >₹94,000 | N/A |

Source: Company Filings, FinScann Analysis

Loading chart...

Market Impact

The MoD-HAL Dornier deal is expected to have a positive impact on HAL's stock (NSE: HAL), particularly given its strong Q3 performance. While the HAL share price has experienced some pressure recently, falling approximately 7% in the last month and 12% in the last three months due to broader market sentiment and concerns over competition, the consistent order inflows and robust earnings provide a strong fundamental backing. The stock traded higher by over 1% on the BSE after the Q3 results and deal announcement on February 12, 2026, closing at ₹4,179.00 apiece.

This contract further de-risks HAL's revenue streams and reinforces its position as a bellwether for the Indian defence sector. The wider Indian aerospace and defence (A&D) sector is experiencing robust growth, driven by aggressive government initiatives for indigenisation, increased capital outlay, and rising export ambitions. The Union Budget 2026-27 allocated a substantial ₹7.85 lakh crore to defence, a 15% increase over the previous year, with a significant ₹2.19 lakh crore earmarked for capital expenditure for modernisation. This sustained government support creates a favorable macro environment for HAL and other defence-related stocks.

Key Takeaways

For investors looking at the Indian defence sector and aerospace stocks, the MoD-HAL Dornier deal highlights several critical points:

Moat Analysis: HAL's Investment Play

HAL possesses a strong competitive moat primarily driven by its strategic importance to India's national security, significant barriers to entry in aerospace manufacturing, and unparalleled government backing.

The Investment Play for HAL is a long-term growth story tied directly to India's escalating defence budget, the 'Make in India' imperative, and a geopolitical landscape that necessitates a robust indigenous defence industry. Investors are looking at HAL as a defensive stock with consistent demand, strong order book visibility, and a beneficiary of strategic national priorities, despite short-term stock price fluctuations. Diversification into civil aviation platforms also offers future growth avenues.

Q: What is the significance of the 'Buy (Indian)' category for this deal? A: The 'Buy (Indian)' category means that the procurement gives preference to Indian-designed, developed, and manufactured products. This directly supports the 'Aatmanirbhar Bharat' and 'Make in India' initiatives, boosting domestic manufacturing, creating jobs, and fostering indigenous technological capabilities within the country's defence ecosystem.

Q: How does this deal impact HAL's overall order book? A: This ₹2,312 crore deal significantly adds to HAL's already substantial order book, which was reported to be over ₹94,000 crore as of early February 2026. This further strengthens the company's revenue visibility and operational outlook for the coming years, extending well into 2032.

Q: Is HAL a good long-term investment given recent stock volatility? A: While HAL share price has experienced some recent volatility due to market sentiment and competition concerns, its fundamentals remain strong. The company benefits from a robust order book, consistent government contracts, a critical role in national defence, and solid Q3 FY26 earnings. Analysts generally view HAL as a strategic pillar of India's defence manufacturing, with long-term growth potential backed by government support and the expanding defence sector. Investors should focus on the underlying data and strategic positioning for long-term decisions.

Q: What are the key drivers for India's defence sector growth in 2026? A: Key drivers include a significant increase in the Union defence budget for FY27 (up 15% to ₹7.85 lakh crore), a strong emphasis on 'Make in India' and 'Aatmanirbhar Bharat', modernization initiatives, rising defence exports, and policy reforms aimed at faster indigenous procurement, such as the draft DAP-2026. These factors are creating a sustained growth trajectory for Indian defence and aerospace companies.

Disclaimer: For information only; not investment advice. Stock market investments carry risks. Please consult a SEBI-registered advisor before investing. FinScann assumes no liability for decisions made based on this report.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

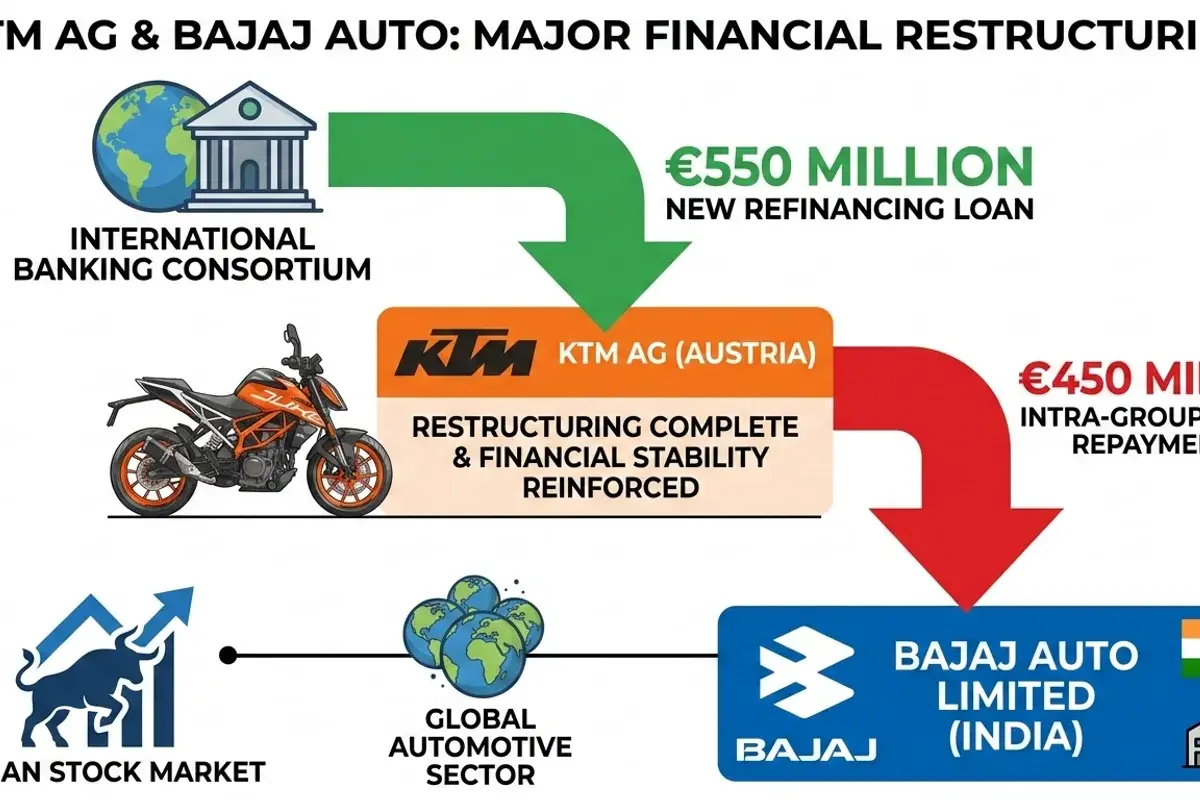

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.