Loading market data...

Tata Motors Passenger Vehicles reported a sharp consolidated loss of ₹3,486 crore in Q3FY26, reversing last year’s strong profitability as a cyber incident at Jaguar Land Rover (JLR) disrupted production, wholesales, and global supply chains. While the overseas shock dragged down consolidated revenue by 26% YoY to ₹70,108 crore, the domestic PV and EV business continued to show resilience with 22% volume growth, reinforcing management’s confidence of a strong recovery in Q4FY26 as JLR operations normalize and domestic demand remains robust.

Tata Motors Passenger Vehicles Ltd (TMPVL) reported a consolidated loss of ₹3,486 crore in Q3FY26, a sharp reversal from a ₹5,406 crore profit in the year-ago period, as revenue fell 26% YoY to ₹70,108 crore. The downturn was driven almost entirely by a severe cyber incident at Jaguar Land Rover that disrupted production, wholesales, and global distribution. Crucially, domestic passenger vehicles and electric vehicle operations remained resilient, posting volume growth of 22% YoY, positioning the company for a sharp Q4 recovery once JLR operations normalize.

The December quarter was always expected to be challenging, but for Tata Motors PV, Q3FY26 turned into a textbook case of how operational shocks can overwhelm otherwise improving fundamentals. While domestic demand remained strong and incentives supported volumes, the scale and timing of the JLR cyber incident dragged consolidated earnings deep into the red.

1. The Q3FY26 Scorecard: A Tale of Two Businesses

Tata Motors PV posted numbers that look alarming at first glance but reveal a split narrative underneath.

Key consolidated metrics:

Net loss: ₹3,486 crore

Revenue from operations: ₹70,108 crore (-26% YoY)

EBIT loss: ₹3,300 crore

Stock price (Q3 close): ₹374.15

Market capitalisation: ₹1.38 lakh crore

P/E ratio: 1.47

Dividend yield: 1.6%

The losses were not demand-driven but event-driven, with management clearly attributing the decline to JLR operations being disrupted by the cyber incident. Domestic operations, by contrast, delivered sequential improvement in volumes, revenue, and margins, highlighting the underlying strength of Tata Motors’ India-focused portfolio.

Shutterstock (Suggested chart: Consolidated revenue vs loss — Q3FY25 vs Q3FY26)

Expert Insight “This was a challenging quarter as anticipated due to the carryover impact of the JLR cyber incident. Domestic business delivered robust revenue and margin improvement QoQ, and we expect performance to significantly improve in Q4,” said Dhiman Gupta, CFO, Tata Motors Passenger Vehicles.

2. The JLR Cyber Incident: How a Technology Failure Became a Financial Shock

The cyber incident at Jaguar Land Rover proved far more disruptive than initially expected.

Key impacts:

JLR revenue: £4.5 billion (-39% YoY)

Production returned to normal only by mid-November

Additional time required to distribute vehicles globally

Loss before tax (JLR): £310 million

The incident triggered a cascading effect across:

Wholesale volumes

Inventory movement

Dealer replenishment cycles

Adding pressure were:

Planned wind-down of legacy Jaguar models

Weak market conditions in China

Incremental US tariffs

Higher variable marketing expenses (VME)

Together, these factors compressed margins and pushed JLR’s EBIT margin guidance for FY26 to just 0%–2%, with free cash outflow projected at £2.2–2.5 billion, reinforcing why Q3FY26 should be viewed as an abnormal quarter rather than a trend signal.

3. Domestic PV & EV Business: Quiet Strength Beneath the Noise

Excluding JLR, Tata Motors’ domestic story was far more constructive.

Domestic PV and EV business performance:

Volumes: 171,000 units (+22% YoY)

Revenue: ₹15,300 crore (+24% YoY)

EBITDA margin: 7% (-80 bps YoY)

EBIT margin: 1.2% (-50 bps YoY)

Volume growth was driven by:

Temporary GST reductions

Continued strength in SUV and EV demand

Strong performance of models such as Nexon, Punch, Tiago and the expanding EV portfolio

Margin pressure came from adverse realisations, commodity costs, fixed expenses, and higher depreciation, partially offset by incentives and operating leverage.

4. Recent and Key Tata Motors Passenger Vehicle Launches

| Model | Powertrain | Segment | Strategic Importance |

|---|---|---|---|

| Tata Punch EV | Electric | Compact SUV | Entry-level EV volume driver |

| Tata Nexon Facelift | ICE + EV | Compact SUV | Core profitability anchor |

| Tata Curvv (Upcoming) | ICE + EV | Coupe SUV | Premiumisation push |

| Tata Harrier EV | Electric | Mid-size SUV | Margin expansion product |

| Tata Sierra (Planned) | Electric | Lifestyle SUV | Brand revival & halo model |

These launches underline Tata Motors’ dual strategy of electrification and SUV dominance, strengthening its positioning in India’s fast-evolving auto market.

5. Stock Reaction & Valuation: Why Markets Stayed Cautious

Despite management’s confident Q4 outlook, Tata Motors stock reacted mildly negative, reflecting:

Uncertainty around JLR recovery timing

Elevated beta of 2.09, indicating high volatility

Investor focus on cash flows rather than accounting profits

Valuation lens:

P/B ratio at 1.10x suggests limited downside if recovery materialises

Low P/E reflects temporarily depressed earnings, not structural decline

Markets appear to be waiting for execution, not promises.

6. Q4 Outlook: Why the Worst May Be Behind

Management expects a sharp improvement in Q4FY26, driven by:

Normalisation of JLR production and wholesales

Continued domestic PV demand

New launches and brand-led actions at JLR

Enterprise missions programme aimed at improving savings and cash flows

Investment guidance remains unchanged, with £18 billion committed over FY24–FY28, reinforcing confidence in Tata Motors’ long-term product and technology roadmap.

7. FAQs

Why did Tata Motors PV report such a large loss in Q3FY26?

The loss was primarily due to a major cyber incident at JLR that disrupted production, wholesales, and global distribution.

Is Tata Motors’ domestic business weak?

No. Domestic PV and EV volumes grew 22% YoY, with revenues up 24%, indicating strong underlying demand.

Will Tata Motors recover in Q4FY26?

Management expects a significant recovery as JLR operations normalise and domestic momentum continues.

Does this loss change Tata Motors’ long-term outlook?

The loss is viewed as event-driven rather than structural. Long-term strategy around SUVs, EVs and premiumisation remains intact.

⚠️ DISCLAIMER: We Are Not Financial Advisors This article is for informational purposes only and does not constitute investment advice. Readers should consult qualified financial advisors before making any investment decisions.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

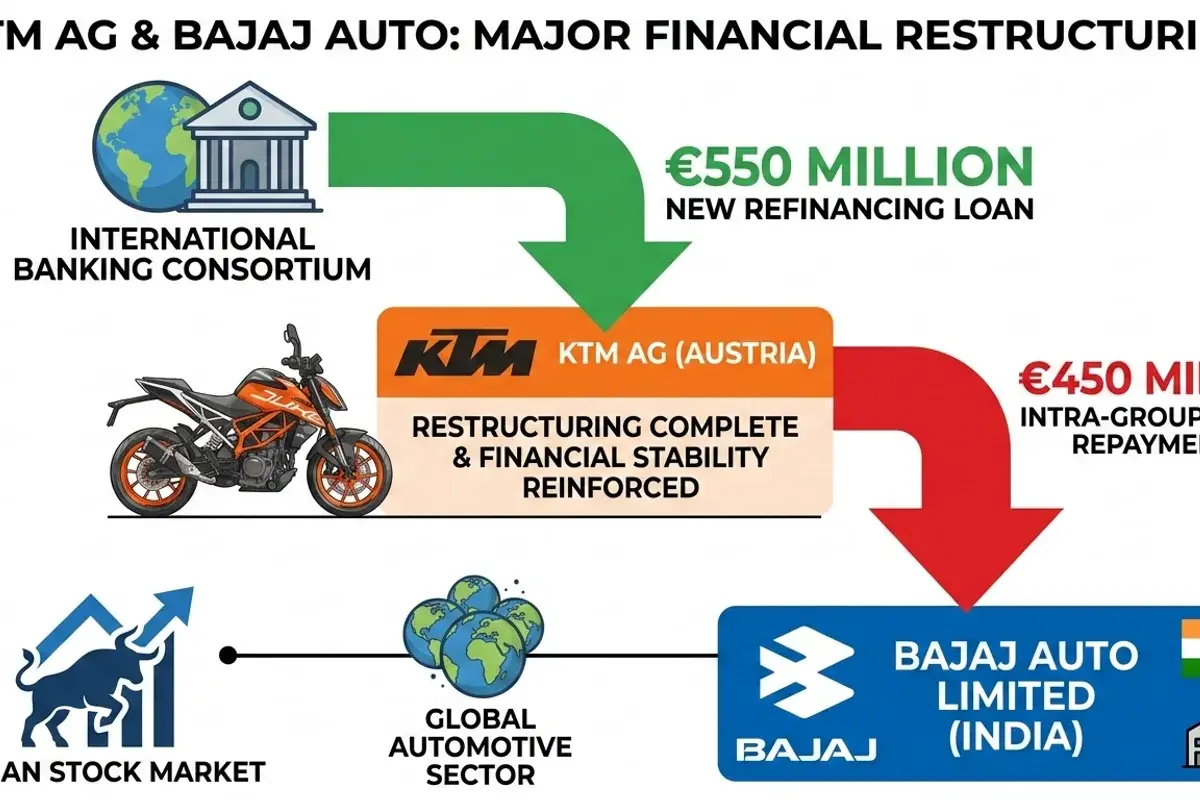

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.