Loading market data...

Sarda Energy & Minerals reports a significant Q3 FY26 profit and revenue decline, grappling with severe margin pressures. FinScann analyzes the impact and future outlook for investors.

Sarda Energy's Q3 Profit Dips Amidst Intense Margin Pressures in Early 2026

Sarda Energy & Minerals Ltd. (NSE: SARDAEN, BSE: 504614) has announced a notable decline in its standalone and consolidated profits and revenues for the third quarter of Fiscal Year 2026, ending December 31, 2025. This downturn primarily stems from persistent margin pressures and challenging market dynamics within the steel and power sectors. The results, released on February 7, 2026, present a mixed picture, with quarterly figures showing contraction despite a strong nine-month performance influenced by an acquisition.

The Catalyst

The primary driver behind Sarda Energy's Q3 profit drop is the severe squeeze on operating margins. The company's consolidated EBITDA saw a significant 15.7% decrease to ₹310.8 crore year-on-year, with EBITDA margins narrowing to 24.36% from 27.95% in the corresponding quarter of the previous year. This compression signals difficulties in converting revenue into profitability, largely attributable to escalating input costs and softer pricing power in its core segments, particularly steel and power.

Broader macroeconomic trends in the Indian steel sector have compounded these pressures. The industry is grappling with declining steel prices and rising costs for crucial inputs like coking coal. Rating agency ICRA projects that despite an estimated 8% growth in domestic steel demand for FY2026, softer steel prices are likely to keep operating margins flat for producers, hovering around 12.5%. The steel market is experiencing a temporary surplus due to increased capacity additions, intensifying the competition and putting a cap on price increases.

Further, the ongoing legal uncertainty surrounding the SKS Power acquisition, despite boosting nine-month results, poses a potential risk. A Supreme Court decision challenging the amalgamation remains pending, adding a layer of concern for investors.

Financial Forensics

Sarda Energy's Q3 FY26 financial performance highlights a divergent trend between its quarterly and nine-month results. While the nine-month performance has been robust, bolstered by the SKS Power amalgamation, the quarterly figures reflect the immediate impact of market headwinds and margin contraction.

On a standalone basis for Q3 FY26, Sarda Energy & Minerals reported a 12.3% decrease in revenue from operations, totaling ₹917.62 crore compared to the previous year. Profit Before Tax (PBT) also saw a 4.3% decline to ₹221.21 crore, and net profit after tax fell by a more substantial 14.3% year-on-year to ₹163.09 crore. Basic and diluted Earnings Per Share (EPS) stood at ₹4.63, down from ₹5.37 in the year-ago period.

The consolidated Q3 FY26 results mirrored this challenging environment, albeit with slightly less pronounced declines in some metrics. Consolidated revenue from operations was ₹1,275.99 crore, a 3.3% decrease year-on-year. While Profit Before Tax (PBT) surprisingly rose by 12.8% year-on-year to ₹254.95 crore, the net profit attributable to owners decreased by 3.5% to ₹190.37 crore. Consolidated EPS was ₹5.40, a slight dip from ₹5.60 in Q3 FY25.

In contrast, the nine-month (9M FY26) consolidated performance demonstrated strong growth, with revenue from operations increasing 30.3% year-on-year to ₹4,436.88 crore. Consolidated Net Profit for the nine months surged by 60.2% year-on-year to ₹947.91 crore. However, the company explicitly noted that these nine-month results are not directly comparable due to the SKS Power amalgamation, which significantly altered the financial landscape.

Here’s a snapshot of Sarda Energy's Q3 FY26 Financial Performance (Consolidated, as of December 31, 2025):

| Metric | Q3 FY26 (₹ Crore) | Q3 FY25 (₹ Crore) | Year-on-Year Change (%) |

|---|---|---|---|

| Revenue from Operations | 1,275.99 | 1,320.00 (approx) | -3.3% |

| EBITDA | 310.8 | 368.6 (approx) | -15.7% |

| EBITDA Margin | 24.36% | 27.95% | -3.59 ppts |

| Profit Before Tax (PBT) | 254.95 | 226.06 (approx) | +12.8% |

| Net Profit | 190.37 | 197.36 (approx) | -3.5% |

| EPS (₹) | 5.40 | 5.60 | -3.57% |

Source: FinScann Analysis of Company Filings and Whalesbook Data

Loading chart...

Market Impact

The market's reaction to Sarda Energy's Q3 results and the broader steel sector challenges has been dynamic. As of February 6, 2026, Sarda Energy (SARDAEN) was trading at ₹529.55 on the NSE. Technically, the stock recently registered a fresh breakout from a descending triangle pattern on the daily chart, accompanied by a surge in volumes, suggesting some bullish momentum in the near term towards the ₹555 level. However, this short-term optimism exists against a backdrop of sectoral headwinds.

The Nifty Metal index has experienced significant pressure, dropping 4.6% on Sunday, February 1, 2026, and a further 2.33% on February 5, 2026, extending a two-day slide after a strong January rally. This volatility is attributed to profit-booking and a macro re-pricing event. While domestic steel demand is projected to grow, the incremental supply in the market and sustained pressure on prices are expected to keep the operating environment challenging for steelmakers in the coming quarters. Investors are closely monitoring the impact of increased input costs, especially coking coal, on the profitability of major players.

Key Takeaways

FinScann Verdict

Sarda Energy & Minerals' Q3 FY26 results reflect the challenging realities of the current market, particularly the relentless pressure on margins. While the strong nine-month performance, amplified by strategic acquisitions, offers some comfort, investors must remain vigilant regarding quarterly profitability and the broader sectoral headwinds. FinScann advises a cautious approach, focusing on the company's ability to manage input costs and pricing power in a competitive environment. The long-term outlook for the Indian steel sector remains stable with robust demand, but the short-to-medium term could see continued volatility and margin challenges.

Q: What caused the decline in Sarda Energy's Q3 profit? A: The primary reason for the decline in Sarda Energy's Q3 profit was intense margin pressure, driven by increased input costs and softer pricing power in its core steel and power segments. Consolidated EBITDA margins narrowed significantly from 27.95% to 24.36% year-on-year.

Q: How did the SKS Power amalgamation affect Sarda Energy's results? A: The SKS Power amalgamation significantly boosted Sarda Energy's nine-month (9M FY26) consolidated revenue and net profit, with revenue up 30.3% and net profit up 60.2% year-on-year. However, the company noted that these nine-month results are not directly comparable to previous periods due to this acquisition. A Supreme Court decision challenging the acquisition remains a key risk.

Q: What is the outlook for the Indian steel sector in 2026? A: The outlook for the Indian steel sector in 2026 indicates healthy domestic demand growth of around 8%. However, increased supply and softer steel prices are expected to maintain margin pressures on producers, with operating margins projected to remain flat around 12.5%. Rising coking coal costs also contribute to the challenging environment.

Q: Should investors be concerned about Sarda Energy's share price? A: While Sarda Energy's share price has shown some recent technical bullish signals, with a breakout from a descending triangle pattern, the fundamental challenges of declining Q3 profitability and ongoing sector-wide margin pressures warrant caution. Investors should closely monitor the company's ability to navigate these challenges and the outcome of the SKS Power legal case.

Q: Where can I find more detailed investor information for Sarda Energy & Minerals Ltd.? A: For more detailed investor information, you can visit the investor relations sections of the Sarda Energy & Minerals Ltd. official website. The company is listed on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE). You can also find filings and news on exchanges like NSE India and BSE India, or financial news portals like The Economic Times and Mint.

Disclaimer: For information only; not investment advice. Stock market investments carry risks. Please consult a SEBI-registered advisor before investing. FinScann assumes no liability for decisions made based on this report.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

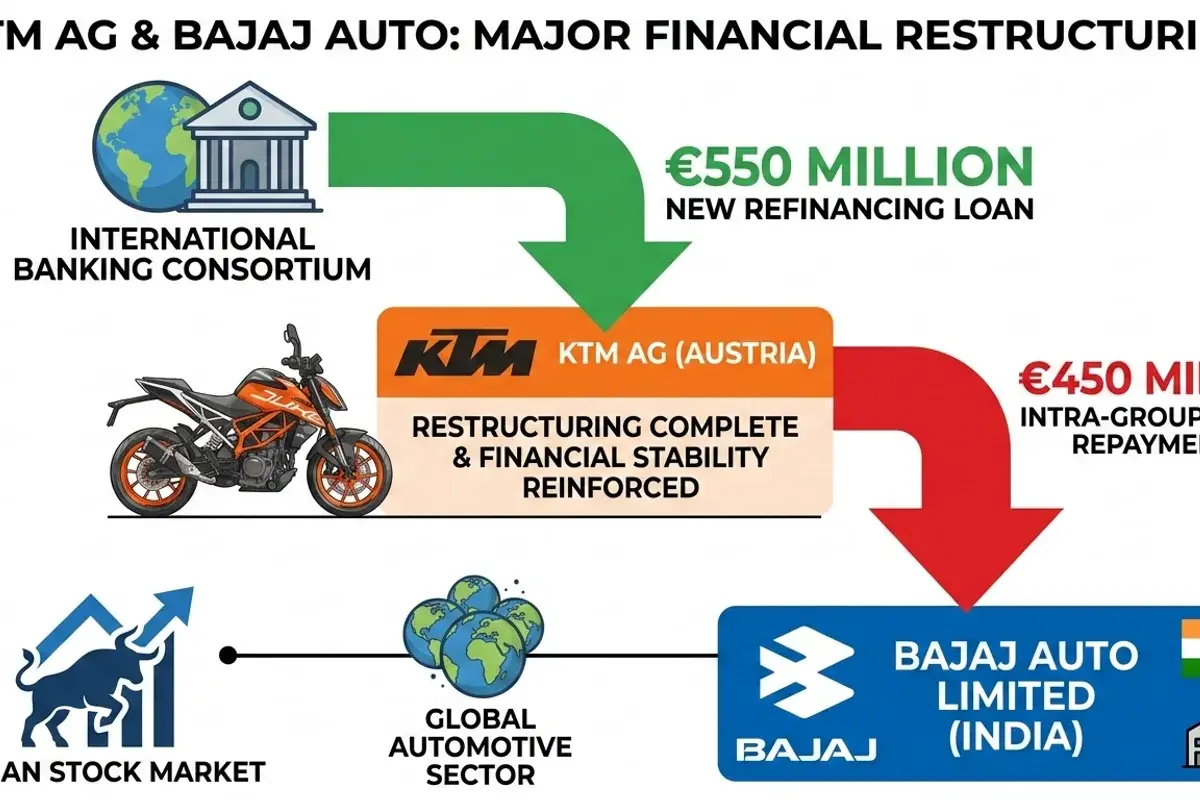

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.