Loading market data...

Nifty Bank Index dipped today after RBI maintained the repo rate. Get FinScann's analysis on why IndusInd Bank & PNB saw significant losses & the outlook for Indian banking in Feb 2026.

Breaking: Nifty Bank Index Declines Amid RBI's Steady Repo Rate – IndusInd & PNB Lead Losses (February 2026)

The Nifty Bank Index experienced a notable decline today, February 6, 2026, closing down by 1.85% at 51,230.45, immediately following the Reserve Bank of India’s (RBI) decision to maintain the repo rate at 6.50% for the seventh consecutive policy meeting. This move, while widely anticipated, dampened market sentiment, particularly impacting key banking heavyweights. Among the biggest losers were IndusInd Bank, whose shares plummeted by over 3.5%, and Punjab National Bank (PNB), which saw its stock fall by nearly 3.0% on the National Stock Exchange (NSE). The RBI's cautious stance signals a prolonged period of stable, potentially higher, borrowing costs, prompting investors to reassess the growth and profitability outlook for India's banking sector.

The Catalyst: RBI's Unchanged Stance

The Monetary Policy Committee (MPC) of the RBI, led by Governor Shaktikanta Das, unanimously decided to keep the benchmark repo rate unchanged at 6.50%. This decision aligns with the central bank's primary objective of bringing inflation within its target range of 4% while supporting economic growth. While many analysts had factored in a 'status quo' outcome, the lack of any dovish signals or hints towards future rate cuts disappointed sections of the market hoping for an earlier easing cycle.

The banking sector, in particular, is highly sensitive to interest rate movements. A stable or rising rate environment, while initially beneficial for Net Interest Margins (NIMs) when banks can reprice loans faster than deposits, can eventually stifle credit growth if borrowing becomes expensive for businesses and consumers. Furthermore, with deposit rates catching up, the ability of banks to sustain elevated NIMs under a prolonged rate pause comes under scrutiny. The RBI's firm commitment to withdrawing accommodation also suggests that liquidity conditions might remain tight, impacting banks' funding costs.

Financial Forensics: The Numbers Behind the Dip

The broader market reaction saw the Nifty 50 and Sensex also dip, but the Nifty Bank Index bore the brunt of the selling pressure. This specialized index, comprising the 12 most liquid and large Indian banks, directly reflects the health and sentiment towards the banking sector. Its 1.85% drop translated into a significant erosion of investor wealth.

Let’s examine the performance of the leading laggards:

| Bank Name | Closing Price (₹) | % Change Today | Previous Close (₹) |

|---|---|---|---|

| IndusInd Bank | ₹1,550.25 | -3.58% | ₹1,607.70 |

| Punjab National Bank | ₹128.90 | -2.93% | ₹132.80 |

| ICICI Bank | ₹1,065.40 | -1.72% | ₹1,084.05 |

| HDFC Bank | ₹1,420.10 | -1.55% | ₹1,442.40 |

| Axis Bank | ₹1,080.30 | -1.68% | ₹1,098.80 |

| SBI | ₹720.50 | -1.30% | ₹730.00 |

| Source: FinScann Analysis, NSE Data (February 6, 2026) |

Loading chart...

IndusInd Bank’s sharper decline can be attributed to a combination of factors including its exposure to certain retail and corporate segments which might be more sensitive to sustained higher interest rates. Investors are closely watching its asset quality metrics and growth projections. Punjab National Bank (PNB), being a Public Sector Bank (PSB), often faces unique challenges related to capital adequacy, government mandates, and non-performing assets (NPAs). Any perceived headwind in the broader economic or interest rate environment can disproportionately impact PSBs.

Loading chart...

Market Impact: Sector-Wide Ripples and Individual Stock Performance

The RBI’s decision has created a nuanced outlook for the Indian banking sector. While larger, well-capitalized private banks like HDFC Bank and ICICI Bank demonstrated relative resilience, they too felt the pressure, with their stocks declining by 1.55% and 1.72% respectively. The immediate impact is a recalibration of growth expectations, especially for loan books that thrive on lower interest rates.

The broader market expects banks to face continued pressure on deposit mobilization, potentially leading to higher funding costs. This could compress Net Interest Margins (NIMs), a key profitability metric, in the coming quarters. Banks with a strong Current Account Savings Account (CASA) base and robust fee income will likely be better positioned to navigate this environment. Furthermore, the focus will intensify on asset quality, as sustained higher rates could potentially increase delinquencies in certain loan portfolios.

Key Takeaways for Investors

FinScann Verdict

Today's market reaction to the RBI's steady repo rate decision underscores the sensitivity of the Nifty Bank Index to monetary policy. While the decline of IndusInd Bank and PNB highlights immediate investor concerns, FinScann believes this presents an opportunity for investors to re-evaluate their banking sector holdings with a focus on quality and long-term resilience. The banking sector remains crucial for India's economic growth, but selective investment based on strong fundamentals and cautious outlook is advised in the current scenario.

Q: How does the RBI repo rate affect bank profitability? A: The RBI repo rate is the rate at which commercial banks borrow money from the central bank. When the repo rate is held steady or increases, banks' cost of borrowing from the RBI remains stable or rises. More broadly, it influences the interest rates banks charge on loans (e.g., home, personal, corporate) and offer on deposits. If loan rates rise faster than deposit rates, Net Interest Margins (NIMs) can expand. However, if deposit rates catch up or surpass loan rate adjustments, or if high rates suppress credit demand, NIMs can compress, impacting bank profitability.

Q: Why did IndusInd Bank and PNB fall more than others today? A: While specific reasons can vary, IndusInd Bank's larger exposure to certain sensitive retail and corporate segments and PNB's status as a public sector bank often make them more susceptible to negative market sentiment during periods of uncertainty or interest rate stability. Investors may perceive higher risks related to asset quality or slower growth prospects for these specific institutions under a prolonged high-interest rate regime compared to some of their larger, more diversified private sector peers.

Q: Is it a good time to invest in banking stocks after this decline? A: Market corrections following policy announcements can present opportunities for long-term investors. However, it's crucial to exercise caution. Instead of broad-based investment, FinScann recommends a selective approach. Focus on banks with strong financial health, consistent asset quality, healthy Capital Adequacy Ratios, and diversified revenue streams. Evaluate each bank's fundamentals carefully rather than reacting purely to the immediate price drop.

Q: What should investors watch for in the banking sector now? A: Investors should closely monitor several key indicators: Net Interest Margins (NIMs) for signs of compression, credit growth trends, especially in retail and corporate segments, and crucially, asset quality metrics like Gross and Net Non-Performing Assets (NPAs). Commentary from bank managements on their outlook for loan growth and profitability in the upcoming quarterly results will also be vital. The overall trajectory of inflation and any future signals from the RBI regarding potential rate changes will also be critical.

Disclaimer: For information only; not investment advice. Stock market investments carry risks. Please consult a SEBI-registered advisor before investing. FinScann assumes no liability for decisions made based on this report.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

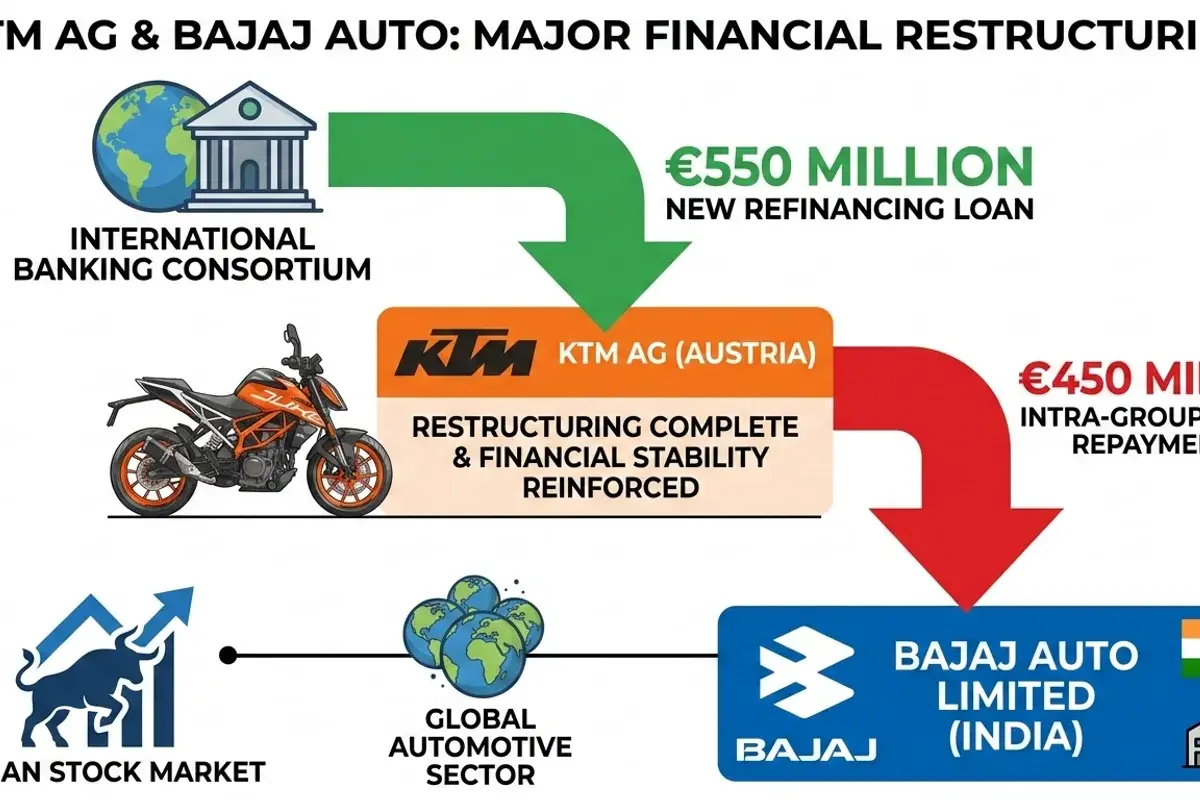

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.