Loading market data...

Synopsis

Maruti Suzuki India Ltd, the country’s largest passenger vehicle manufacturer, delivered a mixed but resilient performance in the December quarter, reporting a 4% year-on-year increase in standalone net profit to ₹3,794 crore despite headwinds from lower export realisations and a one-time labour-related provision. The company’s revenue surged 29% year-on-year to an all-time quarterly high of ₹49,891 crore, driven by robust domestic demand, a sharp recovery in the small car segment, and improved pricing.

While profitability came in slightly below market expectations, strong volumes, record sales, and sequential improvement in earnings underline Maruti Suzuki’s continued dominance in India’s passenger vehicle market.

Loading chart...

Maruti Suzuki Q3 FY26: Key Financial Highlights

| Particulars | Q3 FY26 | Q3 FY25 | YoY Change |

|---|---|---|---|

| Revenue from operations | ₹49,891 crore | ₹38,752 crore | +29% |

| Profit after tax (PAT) | ₹3,794 crore | ₹3,659 crore | +4% |

| EBITDA trend | Moderate growth | — | Margin pressure |

| One-time provision | ₹594 crore | — | Labour code impact |

On a quarter-on-quarter basis, Maruti Suzuki posted a strong rebound:

This sequential improvement reflects stronger festive demand, improved product mix, and operating leverage from higher volumes.

Domestic Sales Drive Growth as Indian Auto Market Recovers

The standout feature of Maruti Suzuki’s Q3 performance was its record-breaking domestic sales volume, signalling a decisive recovery in India’s passenger vehicle market.

The company benefited significantly from the 18% GST bracket small-car category, where affordability, improving consumer sentiment, and better financing availability boosted demand.

Models such as Swift, Baleno, Brezza, and Grand Vitara continued to see strong traction, reinforcing Maruti Suzuki’s leadership across mass-market and compact SUV segments.

Total Sales Touch Record 667,769 Units Despite Export Weakness

Maruti Suzuki’s total sales, including exports, climbed to a record 667,769 units in the December quarter, compared with 566,213 units in the same period last year.

| Sales Mix | Q3 FY26 Units | Q3 FY25 Units |

|---|---|---|

| Domestic sales | 564,669 | 466,993 |

| Exports | ~103,100 | 99,220 |

| Total sales | 667,769 | 566,213 |

While domestic volumes surged, export growth remained muted, and lower export realisations weighed on margins. Currency volatility and competitive pressures in overseas markets limited upside from exports during the quarter.

Why Profit Growth Lagged Revenue Growth

Despite a sharp jump in revenue, Maruti Suzuki’s net profit growth remained modest. Several factors impacted profitability:

These factors offset the benefits of strong domestic volumes and operating leverage, resulting in a smaller-than-expected profit increase.

Labour Code Provision: A One-Time Hit

A key drag on reported profitability was a ₹594 crore one-time provision linked to India’s newly implemented labour codes. Management clarified that this is a non-recurring adjustment, aimed at aligning employee-related liabilities with updated regulations.

From an investor perspective, this provision is viewed as:

As a result, analysts are largely adjusting earnings models to normalise this impact.

GST Reform Acts as Structural Tailwind

While near-term margins faced pressure, the company highlighted GST reforms as a longer-term positive for the industry. Lower tax incidence on certain vehicle categories has improved affordability and widened the addressable market, especially in entry-level cars.

This structural shift is helping revive demand in segments that had been under pressure for several years.

Stock Market Reaction: Volatile but Recovering

Maruti Suzuki shares witnessed a volatile trading session following the earnings announcement.

The recovery indicates that while earnings missed some expectations, investors remain constructive on the company’s long-term growth story and market leadership.

Segment-Wise Performance: What Worked, What Didn’t

What Worked Well

What Remains a Challenge

Industry Context: Auto Sector Shows Signs of Sustained Recovery

Maruti Suzuki’s performance reflects a broader recovery in the Indian automobile sector, supported by:

Passenger vehicle penetration in India remains low compared to global peers, leaving room for structural long-term growth.

Outlook: What Lies Ahead for Maruti Suzuki

Looking ahead, investors will track several key factors:

Management remains optimistic about demand, especially in entry-level and compact SUV categories, while continuing investments in hybrid technology and future mobility solutions.

What This Means for Investors

For investors, Maruti Suzuki’s Q3 results offer several takeaways:

Long-term investors may view earnings-related volatility as an opportunity to reassess valuations rather than a fundamental concern.

Final Takeaway

Maruti Suzuki’s Q3 FY26 results underline the company’s ability to deliver record sales and strong revenue growth even amid margin pressures and regulatory adjustments. While profitability growth was modest, the core business remains healthy, demand trends are improving, and structural tailwinds continue to support the long-term outlook.

As India’s auto market recovers, Maruti Suzuki remains firmly positioned as the undisputed leader, with scale, brand strength, and distribution acting as powerful competitive advantages.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

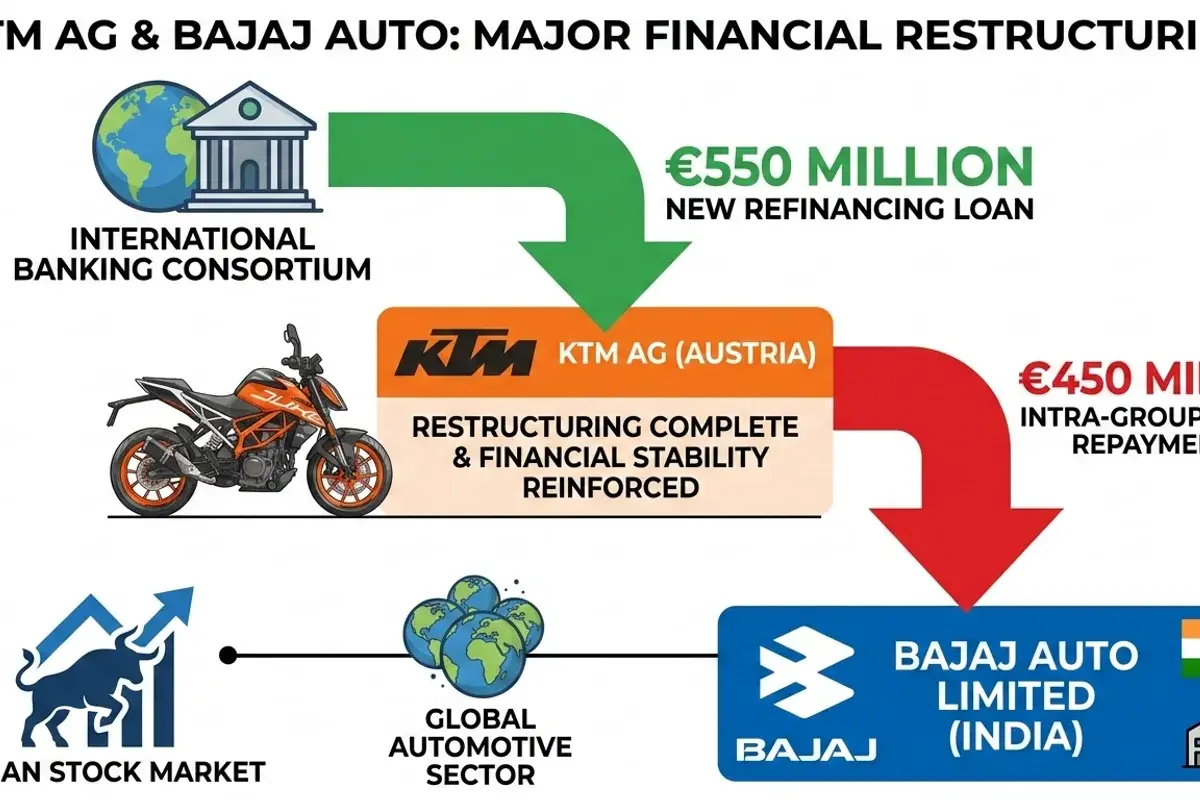

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.