Loading market data...

Introduction: A Defining Quarter for India’s Steel Major

JSW Steel Ltd delivered a blockbuster financial performance in Q3 FY26, reporting a 198.33% year-on-year jump in consolidated net profit to ₹2,139 crore for the quarter ended December 31, 2025.

For a sector known for cyclicality, volatility in raw material prices, and sensitivity to global demand trends, this quarter stands out as a clear demonstration of operational resilience and strategic execution. While the Indian steel industry continues to face cost pressures, geopolitical uncertainty, and fluctuating commodity cycles, JSW Steel has managed to expand margins, improve profitability, strengthen its balance sheet, and streamline its corporate structure—all in a single quarter.

This performance places JSW Steel firmly among the top-performing large-cap metal stocks in India, reinforcing its reputation as a well-managed, execution-focused industrial major.

This article breaks down what drove the massive profit surge, how JSW Steel outperformed peers, what the numbers reveal about demand strength, cost efficiency, and capital discipline, and how investors should interpret the stock’s performance going forward.

Q3 FY26 Performance Snapshot: Key Numbers at a Glance

| Metric | Q3 FY26 | Q3 FY25 | YoY Change |

|---|---|---|---|

| Net Profit (Consolidated) | ₹2,139 crore | ₹717 crore | +198.33% |

| Revenue from Operations | ₹45,991 crore | ₹41,378 crore | +11.1% |

| EBITDA | ₹6,496 crore | ₹5,582 crore | +16.4% |

| EBITDA Margin | 14.12% | 13.48% | +64 bps |

| Standalone Net Profit | ₹757 crore | — | Impacted by exceptional item |

The data clearly highlights one key insight: profit growth far outpaced revenue growth, reflecting operating leverage, disciplined cost management, and superior execution.

Profit Explosion Explained: Why Net Profit Nearly Tripled

The nearly three-fold jump in net profit was not driven by a single factor. Instead, it reflects a structural improvement in JSW Steel’s operating model.

Key contributors included:

• Strong domestic steel demand • Improved price realisation • Optimised operational efficiencies • Strict control over fixed and variable costs • Sustained EBITDA margin expansion

Unlike earlier commodity cycles where profits surged primarily due to pricing, this quarter’s performance reflects quality earnings growth driven by efficiency and scale, not just market conditions.

Revenue Growth: Domestic Demand Continues to Anchor Performance

JSW Steel’s consolidated revenue from operations rose 11.1% year-on-year to ₹45,991 crore, supported by robust domestic demand.

India’s infrastructure expansion, stable construction activity, and steady demand from:

• Automotive manufacturers • Capital goods companies • Engineering and industrial segments

provided a reliable demand base.

The company also benefited from better product mix and higher utilisation, allowing revenue growth without margin dilution.

Loading chart...

EBITDA Performance: Margin Expansion Despite Cost Volatility

One of the most impressive highlights of the quarter was the 16.4% rise in EBITDA to ₹6,496 crore, alongside margin expansion to 14.12% from 13.48% a year earlier.

This came despite volatility in raw material prices, particularly coking coal and iron ore.

Margin improvement reflects:

• Better procurement planning • Energy efficiency initiatives • Operational optimisation at plant level • Tight cost controls

In a capital-intensive business, margin expansion is a strong signal of management quality.

Standalone Results: Exceptional Item Masks Core Strength

On a standalone basis, JSW Steel reported a net profit of ₹757 crore.

Standalone results were impacted by an exceptional item of ₹338 crore, arising from the implementation of new labour codes, which increased employee benefit obligations.

Important points for investors:

• The impact is one-time in nature • It does not reflect operational weakness • It does not alter long-term earnings potential

Core operational performance remains solid and resilient.

Strategic Acquisition: Enhancing Raw Material Security

On December 3, 2025, JSW Steel completed the 100% acquisition of Saffron Resources Private Limited for ₹681 crore.

This acquisition strengthens:

• Backward integration • Raw material security • Cost predictability • Long-term margin stability

In the steel industry, control over inputs directly enhances earnings visibility, especially during commodity cycles.

Subsidiary Mergers: Streamlining Operations and Capital Efficiency

The Board approved the merger of several subsidiaries into JSW Steel, including:

• Amba River Coke • Monnet Cement • JSW Retail and Distribution

These moves aim to:

• Simplify corporate structure • Improve transparency • Reduce operational complexity • Enhance capital efficiency

Over time, this consolidation can improve return ratios and valuation stability.

Balance Sheet Strength: Discipline in a Capital-Intensive Industry

JSW Steel maintained a healthy and stable balance sheet.

| Indicator | Value |

|---|---|

| Debt–Equity Ratio (Standalone) | 0.77 |

| Inventory Turnover | 84 days |

| Trade Receivables Turnover | 17 days |

These metrics highlight strong working capital management, a key differentiator in cyclical industries.

Stock Market Reaction: Why Shares Fell Despite Strong Results

Despite stellar earnings, JSW Steel shares closed 1.60% lower at ₹1,165.40.

Reasons include:

• Short-term profit booking • Broader market sentiment • Valuation sensitivity in metal stocks

Notably, the stock has gained over 25% in the past year, outperforming the broader market.

Short-term price moves should be separated from fundamental strength.

Additional High-Engagement Insight: What This Means for Long-Term Investors

For long-term investors, Q3 FY26 reinforces key themes:

• JSW Steel is managing cycles effectively • Margin resilience is improving structurally • Strategic integration is enhancing stability • Capital discipline remains intact

This quarter strengthens the narrative that JSW Steel is evolving from a pure cyclical play into a more resilient industrial leader.

Industry Context: Why JSW Steel Continues to Outperform

While the steel sector faces:

• Global demand uncertainty • Input cost volatility • Energy price pressures

JSW Steel delivered:

• Revenue growth • Margin expansion • Sharp profit acceleration

This highlights scale advantage, execution efficiency, and strategic foresight.

Forward Outlook: Key Triggers Ahead

Key variables to monitor:

• Domestic infrastructure spending • Steel price movements • Raw material cost trends • Integration benefits from acquisitions • Operational efficiency gains

If current trends persist, earnings visibility remains strong.

Risks Investors Should Monitor

Potential risks include:

• Global steel price corrections • Sharp increases in raw material costs • Policy or regulatory shifts • Macroeconomic slowdown

However, JSW Steel’s scale and balance sheet strength provide resilience.

Frequently Asked Questions

Why did net profit rise sharply?

Due to higher EBITDA, margin expansion, and operational efficiency.

Did exceptional items affect results?

Yes, but only as a one-time labour-related provision.

Is the balance sheet healthy?

Yes, with disciplined leverage and working capital control.

Why did the stock decline post-results?

Short-term profit booking and sentiment-driven moves.

Is JSW Steel a long-term story?

The company remains well-positioned in India’s infrastructure-led growth cycle.

Conclusion: A Quarter That Reinforces Confidence

JSW Steel’s Q3 FY26 performance is not just a profit surge—it is a statement of execution strength, strategic clarity, and financial discipline.

With profits nearly tripling, margins improving, acquisitions strengthening integration, and balance sheet stability intact, the company has reinforced its position as a core player in India’s steel ecosystem.

For investors, this quarter confirms that JSW Steel is not merely riding a cycle—but actively shaping its outcomes.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

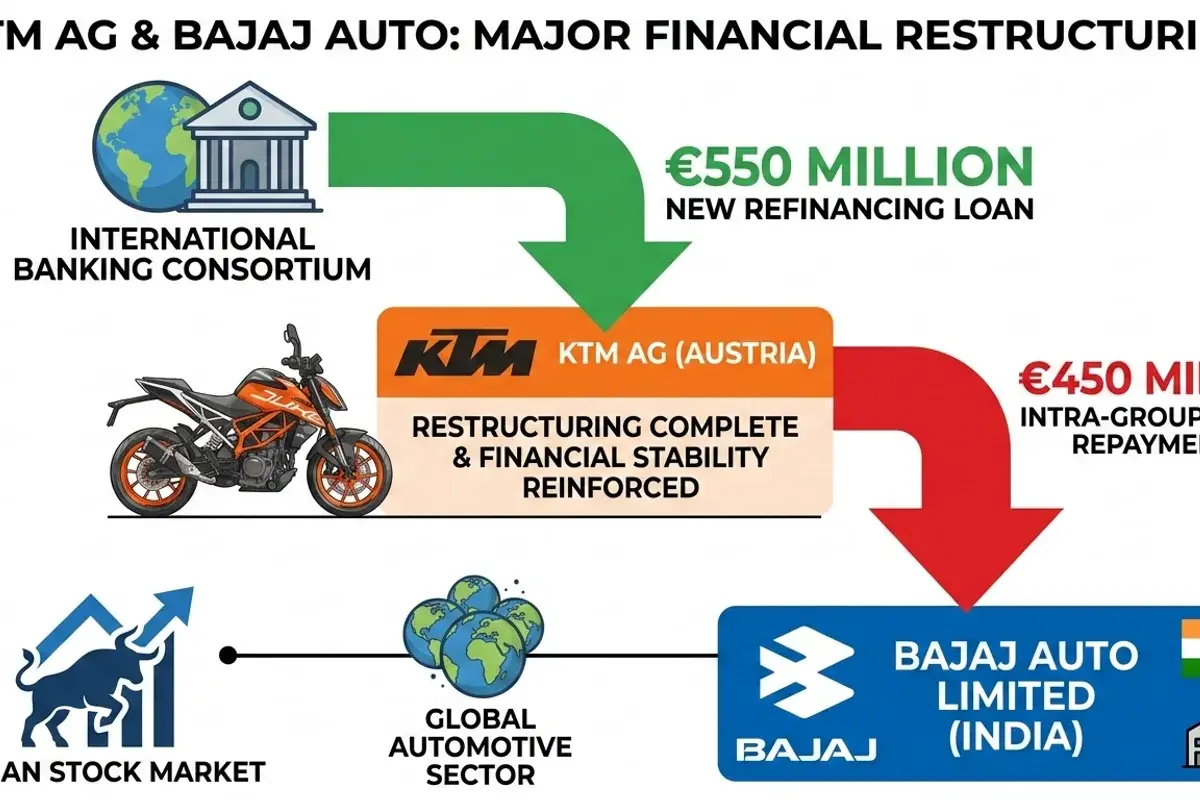

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.