Loading market data...

Indigo Paints has attracted investor attention after Motilal Oswal reiterated a Buy rating with a ₹1,400 target. While Q3 FY26 revenue growth remained modest at 3% YoY, demand has improved significantly since November 2025 with double-digit value growth. For investors, the stock represents a play on decorative paint demand recovery, though competitive pressures remain a key risk.

Synopsis: Indigo Paints has come into focus after Motilal Oswal Financial Services reiterated a Buy rating with a target price of ₹1,400. Despite muted Q3 FY26 revenue growth of 3% YoY, the company reported improving demand trends from November 2025 onward, with double-digit value growth. For investors, the stock represents a play on the recovery of the decorative paints cycle, though competitive intensity remains a key monitorable.

Loading chart...

India’s decorative paints industry is closely linked to housing demand, renovation cycles, and festive-season consumption. After a period of muted demand and seasonal disruptions, early signs of recovery are emerging across the sector. Among the companies drawing investor attention is Indigo Paints, a fast-growing player in the decorative paints space.

The stock has come into focus after Motilal Oswal Financial Services reiterated a bullish stance, citing improving demand trends and long-term growth potential.

Indigo Paints reported 3% year-on-year standalone sales growth in Q3 FY26, though this came on a weak base, as reflected in stock updates on Moneycontrol.

| Metric | Performance |

|---|---|

| Standalone sales growth | +3% YoY |

| Consolidated sales | ₹360 crore |

| Consolidated growth | +5% YoY |

| Subsidiary (Apple Chemie) growth | +32% YoY |

| Stock price (recent) | ~₹976 |

The relatively muted revenue growth was attributed to:

While the quarter started slow, demand showed a clear improvement from November 2025.

This trend indicates early signs of sector recovery, especially in the decorative paints segment.

Indigo’s subsidiary, Apple Chemie, delivered strong growth.

| Segment | Growth |

|---|---|

| Apple Chemie sales | +32% YoY |

This growth helped support consolidated numbers despite muted core demand early in the quarter.

Despite limited pricing power in the near term, the company expects:

This suggests improving volume traction rather than price-led growth.

Motilal Oswal Financial Services has reiterated a Buy rating on the stock.

| Parameter | Value |

|---|---|

| Target price | ₹1,400 |

| Valuation basis | 35× Dec’27E EPS |

| Investment view | Demand-recovery play in paints sector |

This implies meaningful upside from current levels if demand recovery sustains.

Investors should monitor:

The changing competitive landscape in the paints sector remains a key monitorable.

Analysts believe Indigo Paints is entering a recovery phase after a weak demand cycle. If the current momentum sustains into FY27, the company could deliver strong volume-led growth, though competitive intensity will remain a critical factor.

Indigo Paints’ investment case currently hinges on demand recovery and volume growth.

Core triggers:

For investors, the stock represents a mid-cap consumption and housing cycle recovery play.

Popular platforms for trading stocks like Indigo Paints:

⚠️ DISCLAIMER: We Are Not Financial Advisors This article is for educational and informational purposes only. Always conduct your own research or consult a certified financial advisor before making investment decisions.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

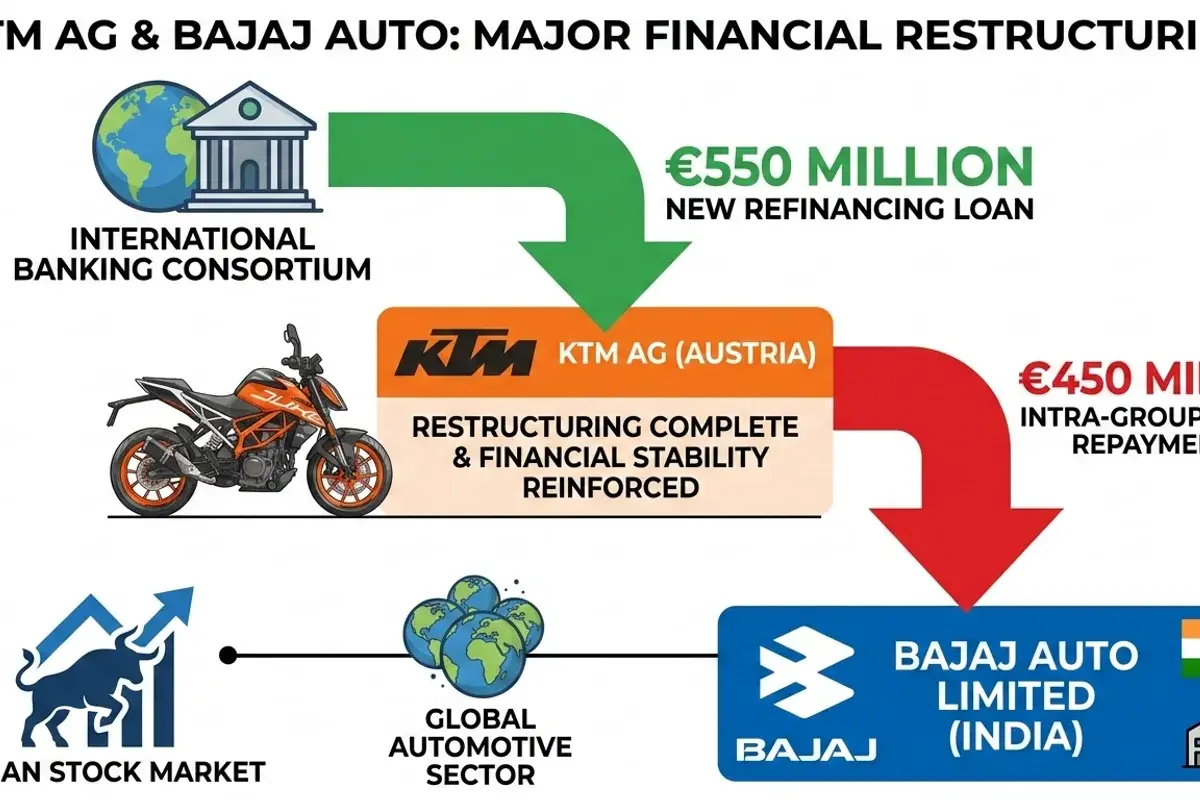

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.