Loading market data...

Cochin Shipyard shares gained over 5% after securing a pivotal ₹5,000 crore Indian Navy contract. Dive into FinScann's analysis of this defence stock's future.

Cochin Shipyard Shares Surge: ₹5,000 Crore Indian Navy Contract Bolsters Defence Stock Prospects – February 2026 Analysis

Cochin Shipyard Ltd (CSL) witnessed a significant rally in its share price, gaining over 5% in early trade on Tuesday, February 17, 2026, following the announcement that it has been declared the lowest bidder (L1) for a crucial ₹5,000 crore contract from the Indian Navy. This strategic deal, confirmed by CSL in a regulatory filing on February 16, 2026, involves the construction of five Next Generation Survey Vessels (NGSV) and marks a substantial boost to the public sector undertaking's robust order book. The news ignited investor interest, with the stock rallying after four consecutive sessions of losses and trading volumes significantly higher than average.

The Catalyst

The trigger for this sharp upward movement in Cochin Shipyard's stock was the official declaration by the Ministry of Defence, New Delhi, that CSL emerged as the L1 bidder for constructing five advanced Next Generation Survey Vessels for the Indian Navy. This contract, valued at approximately ₹5,000 crore, is a testament to CSL's specialized capabilities in naval shipbuilding and its critical role in India's "Atmanirbhar Bharat" (self-reliant India) defence initiative. The final award of the contract remains subject to the satisfactory completion of necessary formalities, which the company expects to update in due course.

Financial Forensics

The ₹5,000 crore Indian Navy contract is a major addition to Cochin Shipyard's already impressive order book, reinforcing revenue visibility for the coming years. As of Q1 FY26 (August 2025), CSL's order book stood at approximately ₹21,100 crore, with a substantial forward pipeline of nearly ₹2.85 lakh crore. This new order significantly bolsters the defence segment, which typically constitutes a major portion of CSL's current orders (65% or ₹13,700 crore as per Q1 FY26 data).

While the company has a strong order book, a deeper dive into recent financial performance reveals mixed signals. In Q3 FY26, Cochin Shipyard reported an 18.3% decline in consolidated net profit to ₹144.67 crore, despite a 17.7% rise in revenue from operations to ₹1,350.41 crore compared to Q3 FY25. Profit before tax (PBT) also saw an 18.6% year-on-year decline. Over the past five years, the company has delivered a sales growth of 5.76%, with a low return on equity (ROE) of 13.5% over the last three years. However, CSL is virtually debt-free, possessing cash reserves of ₹3,021.22 crore as of February 2026, indicating strong financial prudence.

Cochin Shipyard Ltd: Key Financial Metrics (Approximate, as of February 2026)

| Metric | Value | Commentary |

|---|---|---|

| Current Market Cap | ₹38,315.09 Cr | Leading player in defence and commercial shipbuilding. |

| Current Share Price | ₹1,575.00 | (High on Feb 17, 2026) |

| 52-Week Range | ₹1,180.20 - ₹2,545.00 | Shows significant volatility. |

| Existing Order Book (Q1 FY26) | ₹21,100 Cr | Provides strong revenue visibility. |

| New Indian Navy Contract | ₹5,000 Cr | Substantial addition, boosting defence segment. |

| Shipbuilding Pipeline | ₹2.85 Lakh Cr | Massive potential for future contracts. |

| Q3 FY26 Revenue Growth YoY | +17.7% | Healthy top-line expansion. |

| Q3 FY26 Net Profit Growth YoY | -18.3% | Pressure on profitability. |

| Debt | ₹23.02 Cr | Virtually debt-free status is a significant strength. |

| Government Holding | 67.91% | Strong backing by the Government of India. |

| Source: FinScann Analysis based on market data and company filings |

Loading chart...

Market Impact

The news of the ₹5,000 crore contract propelled Cochin Shipyard shares to an intraday high of ₹1,575.00 on the BSE, marking a 7.27% increase. This strong performance highlights renewed investor confidence in India's defence sector, particularly in public sector undertakings (PSUs) benefiting from the government's aggressive indigenisation drive. The broader Indian equity market, represented by the BSE Sensex and NSE Nifty 50, showed mixed movements on February 17, 2026, after an initial negative open, making CSL's individual surge particularly notable. Defence stocks are generally attracting considerable investor attention, driven by geopolitical uncertainties and India's long-term commitment to self-reliance in military hardware.

Moat and Investment Play

Cochin Shipyard possesses a significant "moat" primarily due to its strategic importance and unique capabilities. As the largest shipbuilding and maintenance facility in India, and one of the few globally capable of building aircraft carriers like the INS Vikrant, CSL holds a near-monopoly in large naval shipbuilding within the country. This inherent advantage, coupled with substantial government ownership (67.91%) and consistent orders from the Indian Navy and Coast Guard, provides a high barrier to entry for competitors. The "Investment Play" here is rooted in India's escalating defence budget (FY26-27 defence outlay is ₹7.84 lakh crore), the ongoing indigenisation push under Defence Acquisition Procedure 2026 (DAP 2026), and growing defence exports. These macro tailwinds ensure a steady pipeline of orders and sustained revenue opportunities for key players like CSL.

Key Takeaways for Investors

FinScann Verdict

The ₹5,000 crore Indian Navy contract is a clear positive for Cochin Shipyard, reinforcing its critical role in India's defence ecosystem and boosting future revenue visibility. While recent profitability has faced challenges, the company's strong order book, strategic importance, and government backing make it a compelling long-term play within the burgeoning Indian defence sector. Investors with a long-term horizon and an appetite for the defence theme may find CSL an attractive proposition, though careful monitoring of execution efficiency and valuation remains prudent.

Q: What is the latest news regarding Cochin Shipyard Ltd? A: Cochin Shipyard Ltd (CSL) has been declared the lowest bidder (L1) for a ₹5,000 crore contract to build five Next Generation Survey Vessels (NGSV) for the Indian Navy. This announcement was made on February 16, 2026.

Q: How does this new contract impact Cochin Shipyard's order book? A: This ₹5,000 crore contract is a significant addition to CSL's existing order book, which stood at approximately ₹21,100 crore as of Q1 FY26. It further enhances the company's revenue visibility for the coming years, particularly in the defence segment.

Q: Is Cochin Shipyard a good investment for the long term? A: CSL benefits from strong government support, a robust order pipeline, and a near-monopoly in large naval shipbuilding in India. However, its valuation currently appears high based on some intrinsic value estimates, and recent profit growth has lagged sales growth. It is considered a good long-term investment by some analysts, given India's focus on indigenous defence. Investors should consider these factors and their own risk appetite.

Q: What are the key drivers for defence stocks like Cochin Shipyard in India? A: The primary drivers include the Indian government's increasing defence budget (FY26-27 defence outlay is ₹7.84 lakh crore), the "Atmanirbhar Bharat" initiative promoting indigenous manufacturing, rising defence exports, and the modernization needs of the Indian Armed Forces.

Q: Has Cochin Shipyard's stock performed well historically? A: Cochin Shipyard shares have delivered multibagger returns of 533% in three years and a staggering 762% over the past five years, as of February 17, 2026.

Disclaimer: For information only; not investment advice. Stock market investments carry risks. Please consult a SEBI-registered advisor before investing. FinScann assumes no liability for decisions made based on this report.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

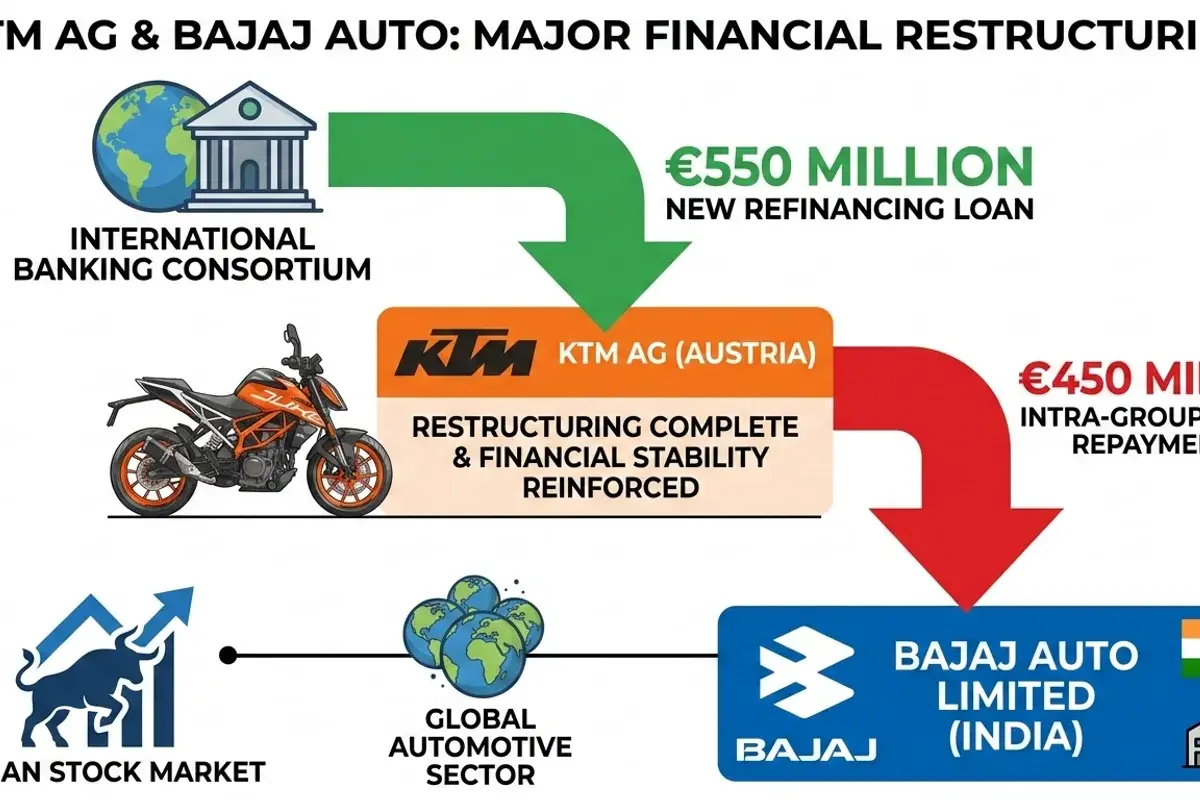

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.