Loading market data...

On January 28, 2026, Axis Bank shares emerged as a top performer in the banking sector, surging over 5% following a "beat-and-raise" December quarter. The primary catalyst was a high-conviction upgrade from JPMorgan, which moved the stock to 'Overweight' with a new price target of ₹1,525, signaling a 15% potential upside.

Axis Bank Stock Analysis: JPMorgan Upgrade and Q3 FY26 Earnings Fuel 15% Upside Potential

MUMBAI — January 28, 2026 — Shares of Axis Bank Ltd surged over 5% in early trade today, hitting an 18-month high after the private lender reported a resilient December quarter (Q3 FY26) scorecard. The rally was supercharged by a high-conviction upgrade from global brokerage JPMorgan, which shifted its rating to 'Overweight' with a bullish price target of ₹1,525.

The upgrade underscores a pivotal shift in the bank's narrative: from managing post-merger integration headwinds to leading the sector in retail asset quality stabilization.

1. Q3 FY26 Results: Profit Beats Estimates

Despite persistent sector-wide margin pressure, Axis Bank delivered a standalone net profit of ₹6,490 crore, surpassing the consensus analyst estimate of ₹6,046 crore.

Loading chart...

2. Asset Quality: The Core Driver of the JPMorgan Upgrade

The most significant "green shoot" in the results was the sharp improvement in asset quality metrics. JPMorgan highlighted that early-bucket retail delinquencies have begun to stabilize, signaling that the worst of the unsecured lending stress may be over.

JPMorgan Forecast: The brokerage has raised its Return on Assets (RoA) estimates for Axis Bank to 1.65% for FY27 and 1.70% for FY28, reflecting a stronger profitability inflection than previously anticipated.

3. Market Context: Banking Sector "Jaw" Performance

Axis Bank’s performance comes at a time when the Nifty Bank index is witnessing a recovery after a volatile 2025. The bank delivered a "positive jaw" (revenue growth outpacing expense growth) for 9MFY26, with cost-to-assets declining to 2.33%.

While Net Interest Margins (NIMs) contracted slightly to 3.64% due to deposit repricing, analysts believe the compression is bottoming out. The bank’s leadership in the UPI space (39% market share) and its digital-first initiatives, like the Google Pay Axis Bank Flex card, continue to drive granular fee income, which grew 12% YoY.

4. Strategic Outlook: Valuation & Targets

With 44 out of 50 analysts covering the stock maintaining a 'Buy' or 'Overweight' rating, the sentiment is overwhelmingly bullish.

| Brokerage | Rating | Price Target (₹) |

|---|---|---|

| JPMorgan | Overweight | 1,525 |

| Elara Capital | Buy | 1,555 |

| Bernstein | Outperform | 1,480 |

| Citi | Buy | 1,463 |

FinScann Take: A High-Quality Compounder

Axis Bank is successfully navigating the transition into a corporate-led growth cycle while keeping its retail house in order. The JPMorgan price target of ₹1,525 implies a 15% upside from current levels. For investors, the key monitoring factor will be the sustainment of the 1.6%+ RoA trajectory and the management of deposit costs in a high-interest-rate environment.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. Stock market investments carry inherent risks. Please consult a SEBI-registered advisor before making investment decisions. FinScann and its authors are not liable for any losses incurred based on this information.

Financial journalist specializing in market analysis, stock research, and investment trends. Dedicated to providing accurate, timely insights for informed decision-making.

Credentials: Experienced financial journalist with expertise in equity markets and economic analysis

The information provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. Finscann does not provide personalized investment recommendations.

For detailed terms and conditions, please read our Disclaimer and Terms of Service.

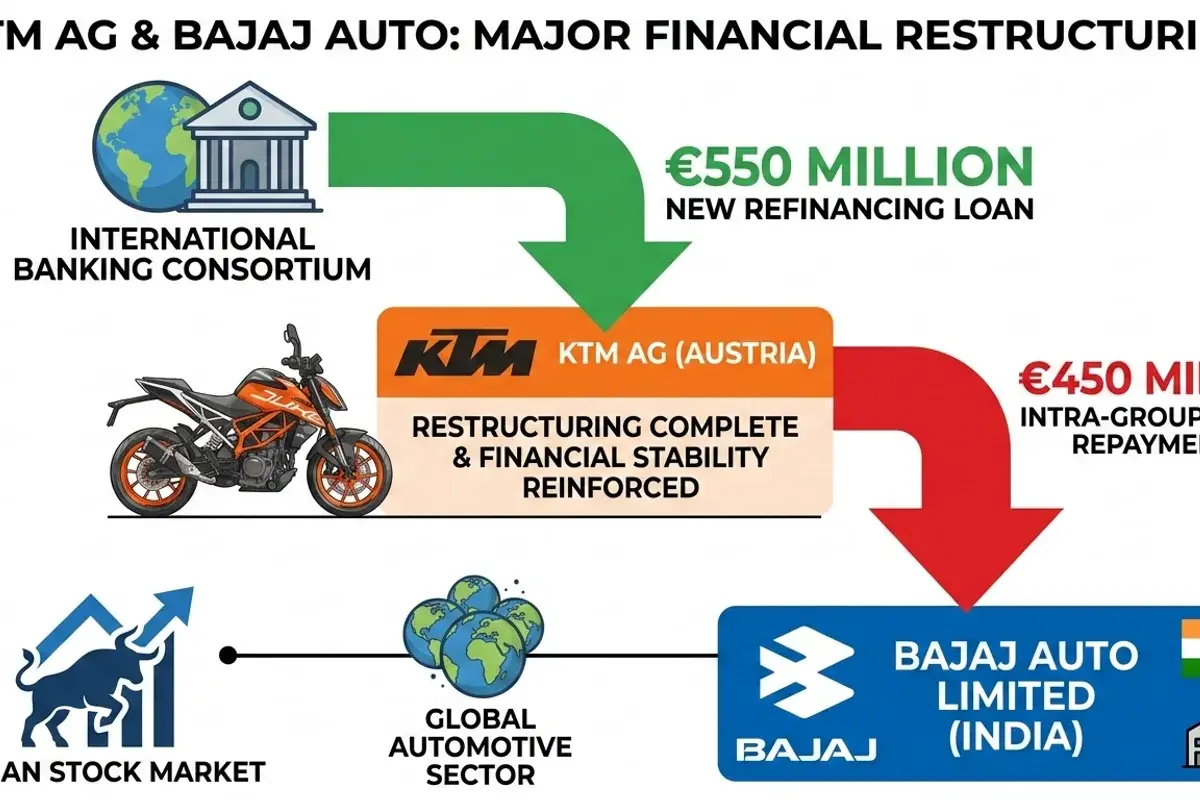

KTM AG repays €450M loan to Bajaj Auto's unit, completing restructuring. FinScann analyzes the financial impact on Bajaj Auto, Pierer Mobility, and...

Tata Elxsi launches DevStudio.ai, an ASPICE-aligned GenAI platform, poised to accelerate automotive software engineering and enhance productivity for...

Waaree Energies bags a significant 300 MW wind power project in Gujarat, marking a strategic expansion and contributing to India's ambitious...

“ABCL is entering a structurally stronger earnings phase, supported by synchronized momentum across lending, AMC, and insurance.

BSE shares surge over 4% after SEBI's critical nod for Sensex Next 30 index derivatives, bolstering its market position and revenue potential.